Proxy Season Highlights, Part Two: What the 2025 No-Action Letter Landscape Tells Us About Preparing for 2026

The 2025 proxy season marked a turning point in the Securities and Exchange Commission’s (SEC) administration of shareholder proposals. Over the course of the season, the staff of the Division of Corporation Finance (staff) received a significant increase in no-action requests under Rule 14a-8 of the Securities Exchange Act of 1934, as amended (Rule 14a-8), granted relief to nearly 70% of requests and, under newly issued Staff Legal Bulletin 14M (SLB 14M), rescinded perceived proponent-friendly guidance in place since 2021. The guidance issued in SLB 14M reverses approximately four years of staff guidance and no-action letter precedent, which had effectively changed how the staff reviewed and analyzed whether shareholder proposals were eligible for exclusion from proxy materials under Rule 14a-8. Although the staff began applying the principles of SLB 14M during the 2025 proxy season, the true impact of SLB 14M and how it will shape future proxy seasons is largely unknown. The 2025 proxy season has provided a preview of what might be on the horizon, but many uncertainties remain about how the staff will apply SLB 14M, especially now that it has had more time to evaluate its application to various arguments for exclusion of shareholder proposals under Rule 14a-8.

Staff Legal Bulletin 14M

On February 12, 2025, the staff published SLB 14M, rescinding previous staff guidance included in SLB 14L – which was published in 2021 and limited the ability to exclude shareholder proposals that raised issues with “broad societal impact” – and reinstating guidance previously rescinded by SLB 14L.1 SLB 14M restored a company-specific, facts-and-circumstances lens to Rule 14a-8(i)(5) (economic relevance) and (i)(7) (ordinary business). SLB 14M confirms that when reviewing company arguments to exclude shareholder proposals under Rule 14a-8(i)(5) and (i)(7), the staff will again look to whether a policy issue is significantly related to the company’s business or focuses on a significant policy issue that has a sufficient nexus to the company, rather than applying the broad societal significance test embedded in SLB 14L.

Although SLB 14M was issued mid-season, its influence was immediate; roughly 30 supplemental letters were filed incorporating fresh company-specific arguments under (i)(5) and (i)(7). Granted relief rates on those supplements were mixed – about 50% under (i)(7) and 33% under (i)(5).

From these decisions, particularly on the (i)(7) letters, there were more than a handful of decisions from the staff denying relief under Rule 14a-8(i)(7) because the company, according to the staff, did not explain why the policy issue raised by the proposal is not significant to the company. For example, several proposals requested that the companies’ boards evaluate and report on how they “oversee risks related to discrimination against ad buyers and sellers based on their political or religious status or views.” In the statements supporting such proposals, proponents argued that the companies censored certain political or religious views in advertising for “brand safety,” rather than protecting “free speech and religious freedom,” such that the issue is one of social policy and “collusive and anti-competitive business behavior,” rather than of controlling the company’s advertising decisions. Many companies argued that the proposal may be excluded pursuant to the ordinary business prong of Rule 14a-8(i)(7) because it relates to the company’s strategy for advertising its products and services and does not focus on a significant social policy issue that transcends the company’s business. The staff denied relief in each of these cases and stated in the response letters that the companies had not explained whether the policy issue raised by the proposal was significant to the company, as required under SLB 14M. In other words, the staff is clearly looking for a more detailed nexus argument when making certain (i)(7) ordinary business arguments, and, in its view, many companies did not overcome that burden.

2025 no-action letter results

The 2025 proxy season saw 371 no-action letters submitted since December 1, 2024, which is a 35% year-over-year increase from the 274 letters submitted in 2024, and a significant increase from the 203 letters submitted in 2023 (when companies appeared less willing to challenge proposals via the no-action letter route after the tumultuous 2022 proxy season where SEC staff denied a significant number of requests post-issuance of SLB 14L in November 2021).2 Although overall grant percentages recovered this season, success under Rule 14a-8 substantive arguments still required detailed company-specific showings.

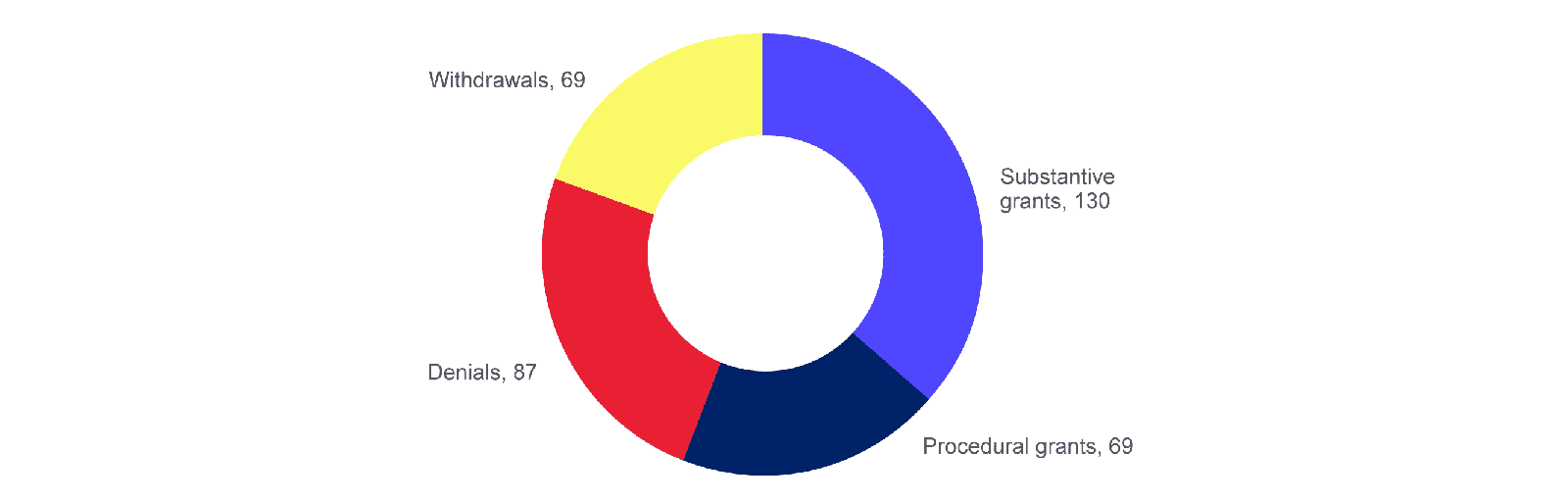

Breaking down the 2025 numbers:

- 371 requests for no-action relief

- 355 decisions by the staff

- 199 grants of relief

- Substantive grants: 130

- Procedural grants: 69

- 87 denials

- 69 withdrawals

Most successful exclusion bases

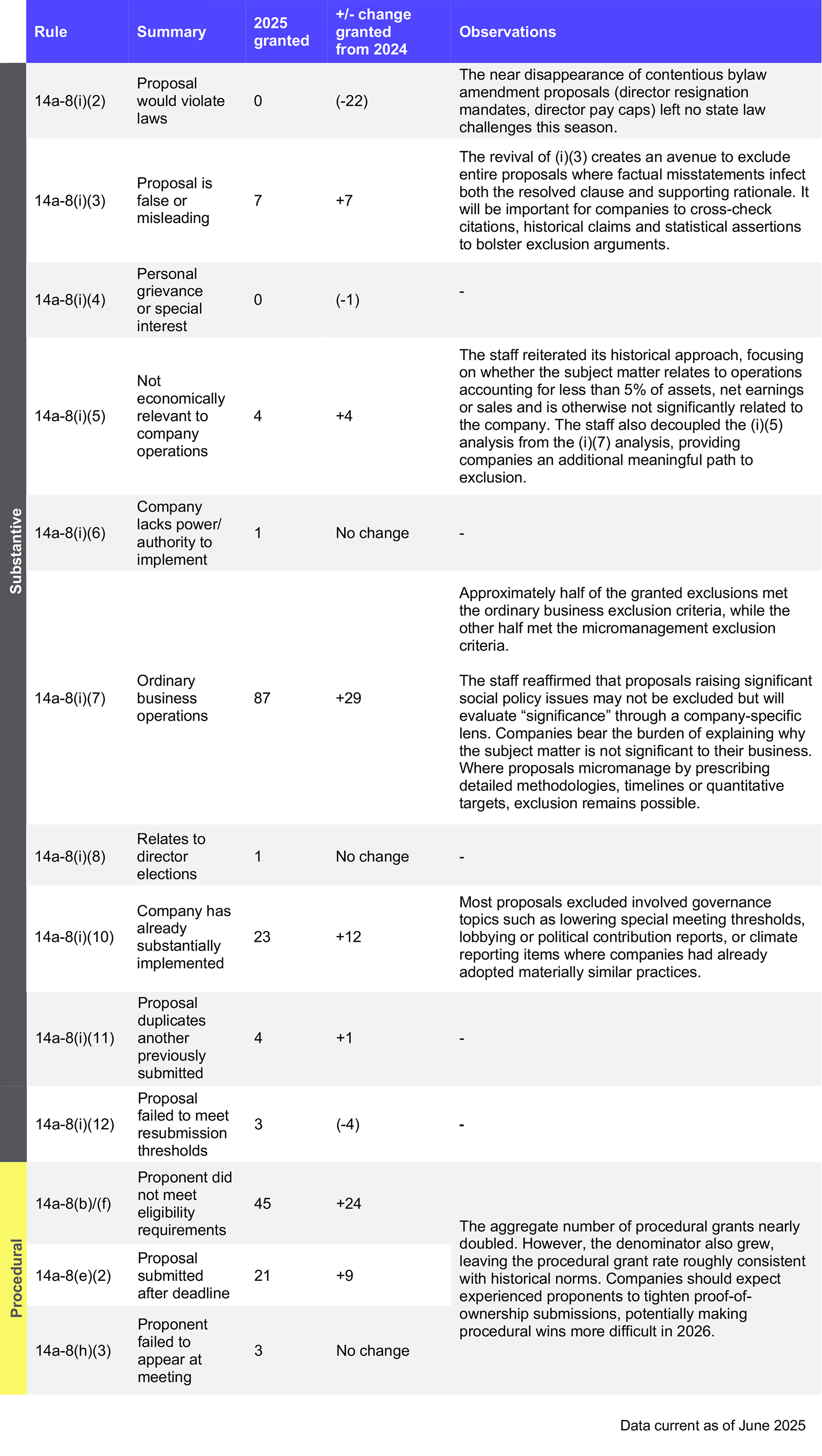

- Ordinary business/micromanagement (Rule 14a-8(i)(7)) – Companies were successful in excluding 87 proposals under this item (up from 58 in 2024) with the grant of no-action letters being split roughly evenly between the two prongs under Rule 14a-8(i)(7): ordinary business and micromanagement. Proposals excluded under the micromanagement prong were generally highly prescriptive and included lobbying disclosure templates and climate reporting mandates dictating methodology or time horizons. Micromanagement letters mapped proposal demands against the board’s existing risk oversight framework to demonstrate usurpation of discretion.

- Substantial implementation (Rule 14a-8(i)(10) – Companies that had already adopted key elements of a proposal were successful in excluding 23 proposals under Rule 14a-8(i)(10) (up from 11 in 2024). This included successful substantial implementation arguments for traditional governance proposals, including proposals requesting the elimination of supermajority voting requirements from company charter documents (eight grants), proposals requesting annual election of directors (five grants) and proposals seeking special meeting rights for shareholders at or below a 20% threshold (one grant). The staff also granted (i)(10) relief for proposals seeking the elimination of diversity, equity and inclusion (DEI) programs and reporting on net-zero activities, goals and policies. The increase in (i)(10) grants in the 2025 proxy season appears to signal a return to the staff’s historical approach to analyzing substantial implementation arguments by focusing on a company’s implementation of the key elements of a proposed action, effectively addressing the core concerns raised by the proposal, or essential objective of the proposal, even if not implementing every detail exactly as requested.

- False or misleading (Rule 14a-8(i)(3) – Companies were successful in excluding seven proposals under Rule 14a-8(i)(3) (up from zero in 2024), including in certain cases where the staff agreed with company arguments that when taken together, the proposal’s resolved clause and supporting statement was premised on objectively false and misleading statements that would materially impact shareholder views of the proposal in violation of Rule 14a-9. For example, the staff granted (i)(3) relief to three companies for proposals requesting the board of directors to conduct an evaluation and issue a report evaluating how excluding religious charities from the companies’ employee gift match program impacts the risks related to religious discrimination against employees. The companies in each case argued that certain statements made in the proponents’ supporting statements were factually incorrect and materially misleading related to company policies and procedures surrounding charitable giving by employees. The significant shift in the staff’s willingness to strike entire proposals where supporting statements contain factual inaccuracies or inflammatory rhetoric will be a key item to watch in the upcoming proxy season. This notable change to the staff’s analysis of Rule 14a-8(i)(3) arguments should encourage companies to scrutinize supporting statements when analyzing potential substantive arguments for exclusion of a proposal.

- Procedural bases (Rules 14a-8(b), (e) and (f)) – Proof-of-ownership and timeliness arguments continue to produce the most reliable wins. Companies were very successful when it came to exclusions on procedural bases by excluding 69 proposals (up from 36 in 2024 and accounting for nearly 35% of all granted no-action letters in 2025). A single shareholder accounted for approximately half of all proposals that included a proof-of-ownership deficiency.

The surge in ownership-proof deficiencies reminds companies that meticulous recordkeeping and prompt deficiency notices remain low-cost paths to exclusion. Rigorous compliance review of any received proposal can yield quick procedural victories. Companies should reexamine calendars for proposal receipt, deficiency notices and response timing. In the upcoming season, all stakeholders will be watching to see if the staff issues global guidance regarding the need to request no-action relief when procedural deficiencies are present.

Full summary of no-action letter results

No-action letter submission reminders

When submitting a no-action letter to the staff, companies should be mindful of certain administrative practice pointers. For example, the staff has publicly stated that when companies provide their proxy print dates to help aid in the timing of staff responses, the staff wants to know the absolute final proxy print date – not the date the company is intending to file the definitive proxy statement on the SEC’s website. In addition, if a no-action letter only includes substantive arguments pursuant to Rule 14a-8, there is no requirement to include copies of any correspondence with the proponent other than the proposal submission. Further, if the no-action letter, and any correspondence submitted along with the letter, includes personally identifiable information (PII), the PII should be redacted before submission of the letter. Finally, the staff has reminded companies to not include a copy of Rule 14a-8 with the no-action letter.

Looking ahead to the 2026 proxy season

The 2025 season confirmed that no-action letter practice will now have a sharper staff focus on detailed company-specific explanations. Companies that integrate 2025 lessons into advance planning, governance enhancements and precision-drafted no-action letters will be best positioned to navigate what promises to be an even more complex 2026 season.

Although SLB 14M was welcome news to many companies this season, the staff’s decision-making process on no-action requests remains opaque. The staff under new Chairman Paul Atkins and a still-to-be-named new director of the Division of Corporation Finance will be crafting its application of SLB 14M and its principles over the coming season, and additional reforms to Rule 14a-8 could be on the horizon. As a result, companies will need to focus on making detailed no-action letter arguments and providing the staff with enough information to help guide them in their decision-making process as whether to grant exclusion, particularly with respect to the (i)(5) economic relevance and (i)(7) ordinary business exclusions. This season provided helpful guideposts for how the staff approaches certain exclusionary arguments, but it will take another full season with SLB 14M before we get a better sense for the outcome of various no-action letter arguments.

It will also take another full season to see how SLB 14M affects the proposals that proponents put forward and the arguments that companies make in response. Because SLB 14M was issued mid-season, 2025 proposals were not drafted with SLB 14M in mind, and as a result, the season saw many more proposals withdrawn than previous years. The 2025 results provide very little insight into whether proponents will submit fewer proposals due to the increased risk of having them excluded, whether companies will submit a significantly larger volume of no-action requests targeting proposals that they previously would not have attempted to exclude, or whether there will be a mix of both. The 2025 season was truly a transition year, and companies should not put too much weight on the statistical outcomes, and focus more on the principles that can be derived from the season generally.

In anticipation of the 2026 proxy season, companies can begin outreach to core institutional holders early, audit gaps in existing disclosures and craft fallback settlement frameworks now.

Notes

- For more information on SLB 14M, see our client alert, SEC Staff Adopts Significant New Guidance Affecting Shareholder Proposals and Engagement.

- For the 2025 season, the staff tracks requests from October 2024 through September 2025; our analysis focuses on the December 2024 to June 2025 window.

Related Contacts

This content is provided for general informational purposes only, and your access or use of the content does not create an attorney-client relationship between you or your organization and Cooley LLP, Cooley (UK) LLP, or any other affiliated practice or entity (collectively referred to as "Cooley"). By accessing this content, you agree that the information provided does not constitute legal or other professional advice. This content is not a substitute for obtaining legal advice from a qualified attorney licensed in your jurisdiction, and you should not act or refrain from acting based on this content. This content may be changed without notice. It is not guaranteed to be complete, correct or up to date, and it may not reflect the most current legal developments. Prior results do not guarantee a similar outcome. Do not send any confidential information to Cooley, as we do not have any duty to keep any information you provide to us confidential. When advising companies, our attorney-client relationship is with the company, not with any individual. This content may have been generated with the assistance of artificial intelligence (Al) in accordance with our Al Principles, may be considered Attorney Advertising and is subject to our legal notices.