Proxy Season Highlights, Part One: Shareholder and Management Proposals

The 2025 proxy season (July 1, 2024 – June 20, 2025, meetings) concluded with a significant drop in the volume of shareholder proposals from the 2024 proxy season’s record high, as environmental and social (E&S) proposals faced headwinds amid shifting political dynamics and evolving stakeholder priorities.

On the management side, shareholder support remained strong across core proposal categories in the 2025 proxy season, with director elections, say-on-pay proposals and equity compensation plan proposals all receiving high levels of approval. The 2025 proxy season underscored the critical importance of proactive stakeholder engagement, intentional disclosure strategies, and careful consideration of the evolving regulatory and political landscape affecting corporate governance priorities.

This alert highlights key trends in both shareholder and management proposals from the 2025 proxy season, including sector-specific trends for tech and life sciences companies.1

Shareholder proposals

The 2025 proxy season saw a notable drop in shareholder proposals in the US market, with Russell 3000 companies receiving 830 proposals, down from a record 983 in the prior year. Social proposals (333, compared to 416 in 2024) and environmental proposals (146, compared to 197 in 2024) were markedly down compared with the previous proxy season, whereas governance proposals – including compensation proposals – remained relatively flat (352, compared to 370 in 2024). Governance proposals recorded stable average shareholder support of 35%, compared to 34% in 2024. Environmental (13% support, compared to 18% in 2024 and 21% in 2023) and social (12% support, compared to 15% in 2024 and 18% in 2023) proposals both recorded lower support than in the prior season.

The overall trends in shareholder proposals continued to be shaped in part by anti-ESG (environmental, social and governance) proponents. These proponents submitted 125 proposals, up from 107 in 2024, though only 73 proceeded to a vote compared to 90 the prior year – reflecting a notable uptick in withdrawals. Average support for these proposals remained low at 2.9%, modestly above the 2.2% support level seen in 2024. The rise in withdrawals may signal that companies are more inclined to negotiate with anti‑ESG proponents, as these proposals often highlight sensitive topics that companies may prefer not to have publicly scrutinized, even if the proposals themselves receive minimal support.

The trends in E&S submissions and support also continued a multiyear decline from COVID-era highs. Although the mid-season publication of Securities and Exchange Commission (SEC) Staff Legal Bulletin (SLB) 14M (to be discussed in more detail in the second part of Cooley’s 2025 Proxy Season Highlights, which will focus on 2025 no-action request trends and the impact of SEC guidance) came too late to impact shareholder proponent strategies during the 2025 proxy season, SLB 14M may contribute to an acceleration of the decline in both submitted and voted proposals in 2026.

As in all years, the data on submitted proposals is inherently incomplete, as it does not capture proposals that were withdrawn by shareholder proponents without public disclosure or those for which no-action relief was not requested. Notably, withdrawals appear to have increased significantly this year, with approximately 160 withdrawals in the 2025 season compared to 66 in the prior season. This trend was particularly pronounced for E&S proposals, with only 251 (52%) going to a vote this season compared to 393 (64%) last season. The increase in withdrawals may reflect greater willingness among shareholder proponents to negotiate with companies, influenced by declining shareholder support for E&S proposals and expectations of unfavorable no-action treatment following the publication of SLB 14M. Given the high number of publicized withdrawals this season, the apparent decline in submitted proposals, particularly those related to E&S matters, may be less significant if there also was an elevated level of nonpublic withdrawals this season.

Environmental and social proposals

A common explanation for declining support for E&S proposals is that the proposals have become increasingly granular and prescriptive. Following years of receiving low-hanging fruit proposals, many of the largest and most visible companies have already addressed foundational ESG expectations (e.g., reporting on greenhouse gas emissions, setting reduction targets and publishing sustainability reports covering key human rights topics), leaving shareholder proponents to choose between submitting more nit-picky follow-up proposals to these companies or focusing on new companies with less direct issue relevance (e.g., climate risk at software companies).

Major investors have cited increased prescriptiveness and decreased relevance as key factors contributing to low levels of support for E&S shareholder proposals in recent years, cautioning that this should not be interpreted as diminished commitment to the underlying issues. An analysis of climate proposals voted on during the 2025 proxy season supports this view, while also pointing to a decline in investor enthusiasm for E&S themes more broadly since their peak in 2020 and 2021. Total climate proposal submissions fell to 95 in the 2025 proxy season, markedly down from 146 in 2024 and 151 in 2023, while average support dropped to 12.7%, continuing a downward trend from 19% in 2024 and 21% in 2023.

To test the prescriptiveness thesis, we analyzed this season’s 51 climate proposals that were focused on the core topics of emissions reporting, target setting and risk disclosures. We categorized these proposals as either “basic,” focusing on foundational actions (e.g., initial Scope 3 emissions reporting or setting an emissions reduction target), or “prescriptive,” focusing on improvements to existing climate activities (e.g., reporting on specific Scope 3 categories, expanding existing targets or supplementing risk reports with disclosures on narrow topics). As expected, “basic” climate proposals received markedly higher support at 17.7%, compared to 9.2% for “prescriptive” climate proposals. However, even support levels for “basic” climate proposals this season were lower than overall support levels for last season’s climate proposals (17.7% versus 19.3%) and were significantly below the 28.4% support seen for last season’s core “basic” climate proposals.

Despite the overall trend of declining support for E&S proposals, certain proposal categories continued to perform well, including human rights and political spending and lobbying, which are discussed in detail below.

With support for climate change and other traditional E&S topics broadly declining, attempts by shareholder proponents to identify a new “hot topic” E&S issue have failed to gain traction. For example, with the introduction of 13 proposals in 2024 related to artificial intelligence (AI) issues, some speculated that widespread concerns with ethical AI usage and workforce impacts would attract shareholder attention. However, with average support of only 22.6% in 2024, shareholder proponents were likely not encouraged to expand AI submissions, as only 11 AI-related proposals were submitted in 2025, with average support of 14.7% for voted proposals.

Human rights and diversity proposals

Human rights-related shareholder proposals remained a focal point in the 2025 proxy season, with 25 submissions and 15 proposals going to a vote – down slightly from the 26 submissions and 19 voted proposals in the 2024 proxy season. These proposals covered a range of topics, including human rights impact assessments, the adoption of comprehensive human rights and respect for Indigenous peoples’ rights. While none of the proposals passed, average support rose to 16%, up from 14% last season, making human rights one of the few social issue categories to see a year-over-year increase in support.

This small uptick is particularly notable amid the broader political environment in which some public companies are reassessing or scaling back public disclosures on various social issues, including diversity, equity and inclusion (DEI) and human rights. While the influence of this modest increase in support remains to be seen, it may offer some encouragement to shareholder proponents considering continued or expanded engagement on human rights matters heading into the 2026 proxy season.

In contrast, proposals focused on workforce diversity and DEI saw a meaningful decline in investor support in the 2025 proxy season, reflecting a broader pullback by investors on politically sensitive social topics in recent months. This decline in support was evident on both sides of the political divide. On the pro‑DEI side, support for proposals requesting racial and gender equity audits, civil rights reporting and related workforce policies continued to soften (15.1% average support, compared to 23.4% in 2024), consistent with the broader retreat from E&S proposals. On the anti‑DEI side, proposals explicitly seeking to roll back DEI programs or related practices also failed to gain traction, continuing to receive very low support (1.5% average support, compared to 1.9% in 2024).

Despite declining support levels, the volume of workforce diversity and DEI proposals increased this season, with 110 submissions (up from 100 in 2024). Notably, 50 pro‑DEI proposals were submitted (compared to 42 last year), suggesting shareholder proponents remain focused on this issue as many companies reevaluate their DEI programs. Withdrawals also increased, with 30 overall withdrawals –including 20 on the pro‑DEI side and 10 on the anti‑DEI side, compared to no withdrawals last year for anti‑DEI proposals. The increase in withdrawals, particularly with respect to anti‑DEI proposals, may reflect companies’ greater willingness to engage and negotiate in order to avoid heightened scrutiny of their workforce practices in the current political environment.

Political spending and lobbying proposals

Political spending and lobbying proposals stood out this proxy season as another area – alongside human rights – where investor support increased and as the only social category to achieve majority support, underscoring that investors continue to distinguish between more and less politically divisive topics when voting. Although the number of voted proposals declined sharply this year (24 in 2025 compared to 66 in 2024), the number of proposals that passed rose to four, up from just one last year.

Average support for these proposals also rose meaningfully to 30.1% in 2025, up from 22.4% in 2024. This upward trend suggests that, even amid broader declines in support for other social issues, investor appetite for enhanced disclosure and oversight of corporate political activities remains strong.

Governance proposals

In stark contrast to E&S proposals, governance proposals continue to be submitted and voted (237 in 2025, compared to 239 in 2024) in high volumes, with average support slightly increasing from 2024 (35% compared to 34%). For the 2025 season, familiar proposal topics predominated, including:

- Proposals requesting the adoption or amendment of shareholder special meeting rights: 79 submitted and 64 voted, with average support of 33.9% (16% passing), compared to 33 submitted and 28 voted, with average support of 44.1% (25% passing) in 2024.

- Proposals requesting the elimination of charter and bylaw supermajority voting provisions (simple majority vote): 42 submitted and 29 voted, with average support of 72% (76% passing) compared to 48 submitted and 40 voted, with average support of 72.6% (75% passing), in 2024.

- Proposals requesting the appointment of an independent board chair: 35 submitted and 28 voted, with average support of 30% (none passing), compared to 48 submitted and 41 voted, with average support of 30.3% (none passing) in 2024.

- Proposals requesting the submission of severance agreements to shareholder votes: 29 submitted and 28 voted, with average support of 24% (none passing), compared to 38 submitted and 35 voted, with average support of 15.3% (none passing) in 2024.

- Proposals requesting the declassification of boards of directors: 24 submitted and 14 voted, with average support of 77.9% (86% passing), compared to 10 submitted and seven voted, with average support of 63% (86% passing) in 2024.

- Proposals requesting the adoption or amendment of resignation policies for directors who fail to receive majority shareholder support: 23 submitted and 15 voted, with average support of 20% (none passing), compared to 44 submitted and 11 voted, with average support of 17.6% (none passing) in 2024.

Forty-six governance proposals passed in the 2025 season, down slightly from 48 in 2024. As in 2024, simple majority vote proposals passed in high numbers in 2025 (22 compared to 30 in 2024), followed by proposals requesting the declassification of boards of directors (12 increasing from only six in 2024) and proposals to adopt or amend shareholder special meeting rights (10 increasing from seven in 2024).

Similar to E&S proposals, shareholders continue to consistently differentiate between “basic” and “prescriptive” proposals, though at much steadier rates year over year. For example, of 64 voted proposals in 2025 related to shareholder special meeting rights, 21 proposals requesting the creation of a right received average support of 48.1% (compared to 50.4% in 2024), compared to average support of 26.3% for 43 proposals requesting amendments to existing rights, such as eliminating holding periods or lowering ownership thresholds (compared to 40.1% in 2024).

Binding bylaw proposals – designed to directly amend a company’s bylaws upon receiving requisite shareholder support – drew attention last proxy season for their novel approach and the governance questions they raised. Notably, proposals seen last year focused on director compensation did not reappear in the 2025 proxy season, and there has not yet been a discernible shift toward deploying this approach on more traditional governance topics. As a result, it remains unclear whether binding bylaw proposals addressing core governance issues would gain meaningful traction with investors if introduced.

Sector trends

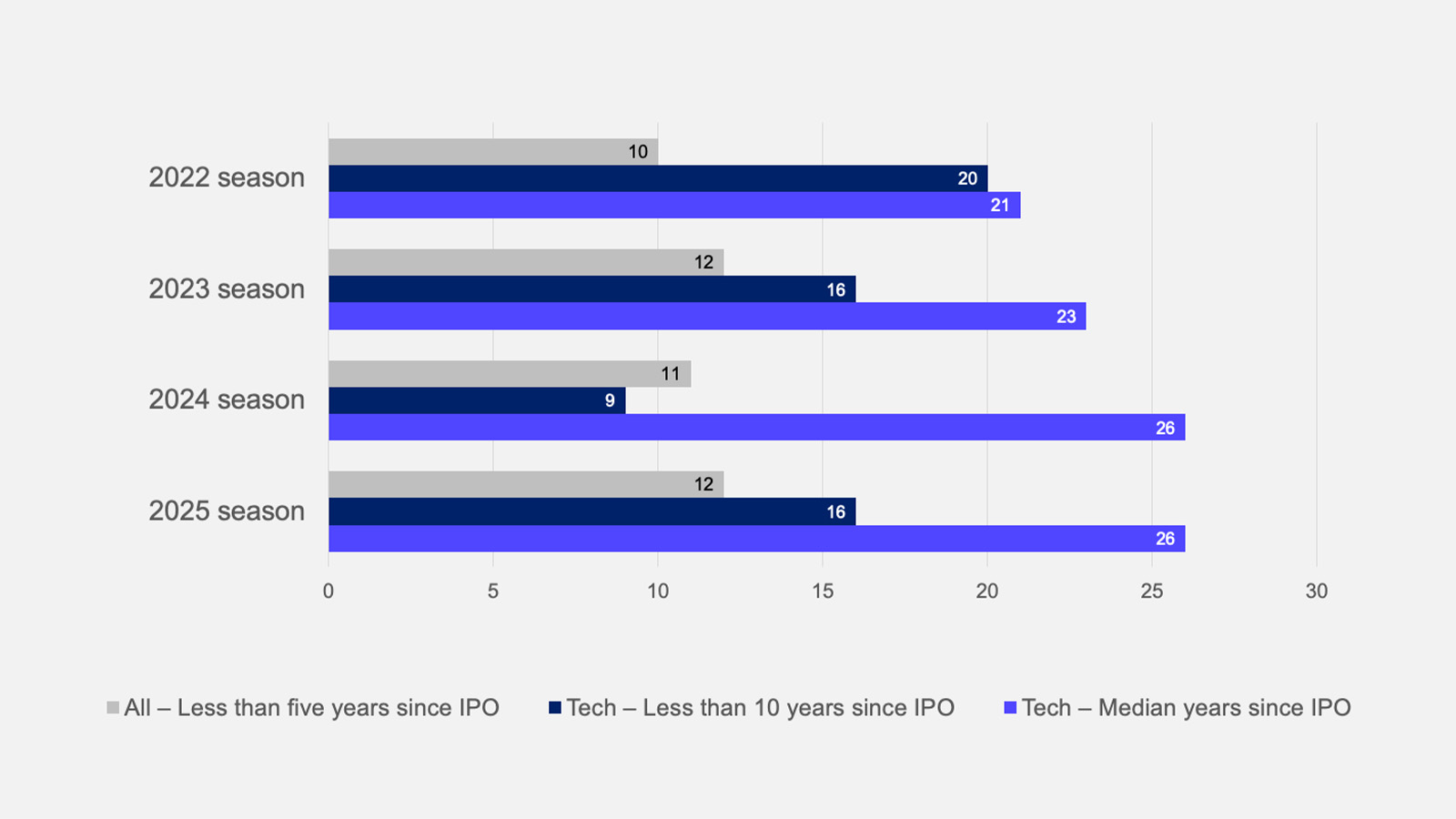

As in prior years, shareholder proposals in 2025 were heavily concentrated among larger-cap mature companies, with only 12 companies less than five years post-initial public offering (IPO) receiving proposals – compared to 11 in 2024, 12 in 2023 and 10 in 2022. For tech-sector companies2, 3, the median shareholder proposal recipient was 26 years post-IPO, compared to 26 in 2024, 23 in 2023 and 21 in 2022. 16 tech companies that went public in the last decade received shareholder proposals in the 2025 season, compared to nine in 2024, 16 in 2023, and 20 in 2022.

Tech Proposals by Market Cap

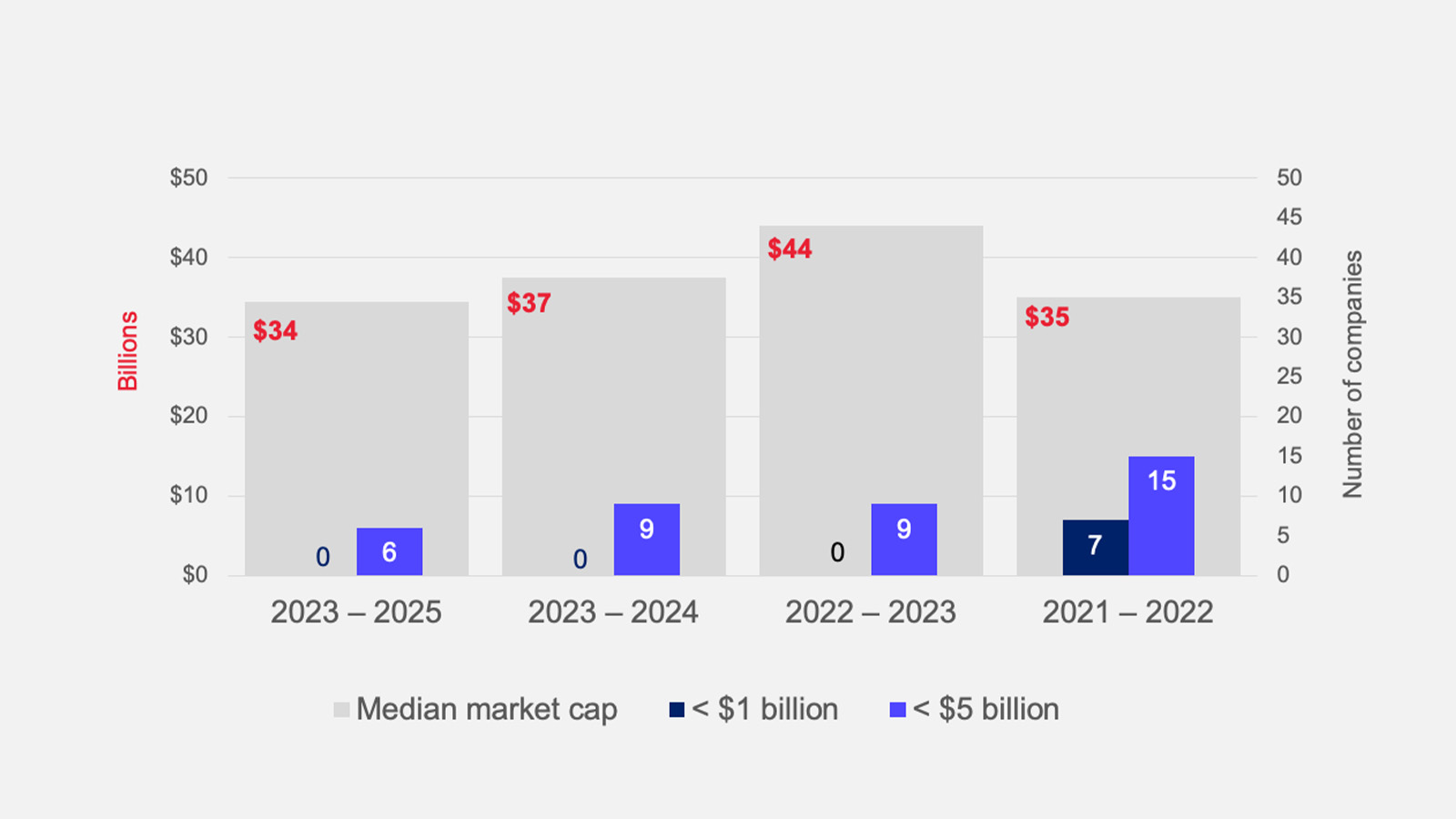

Tech-sector proposals remain focused on large-cap issuers, with a median market cap of $34 billion for proposal recipients in the 2025 season, compared to $37 billion in 2024, $44 billion in 2023 and $35 billion in 2022. As in 2023 and 2024, no tech-sector companies under $1 billion received proposals, unlike in 2022, when proposals were submitted to five such companies. Mid-cap tech companies continue to receive a moderate number of proposals, with six receiving proposals in 2025, compared to nine companies with a market cap under $5 billion in both 2024 and 2023, while in 2022, 15 such companies received proposals.

Tech proposals by category

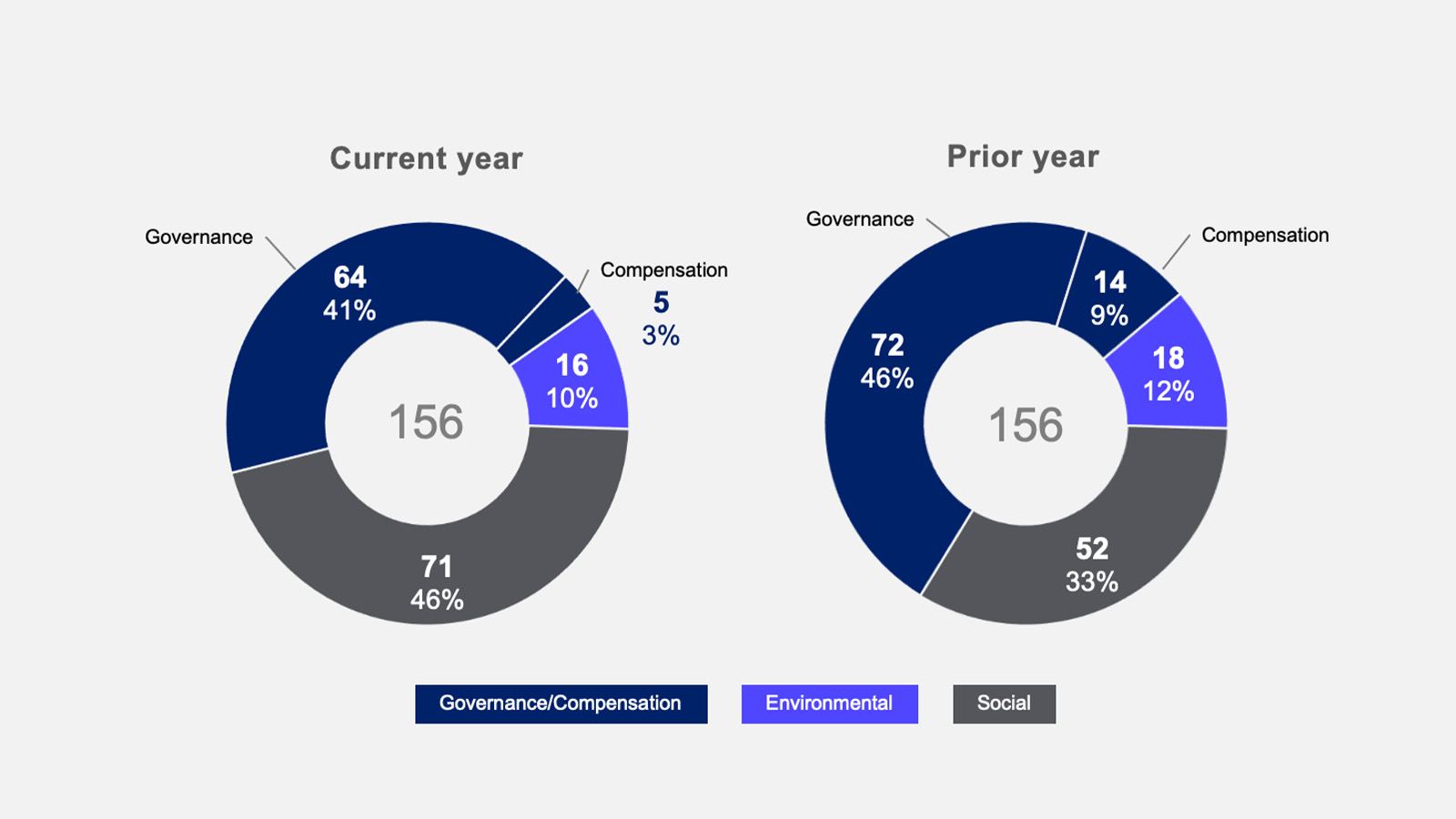

Governance proposals (42%) – including 20 special meeting right proposals, seven simple majority vote proposals, seven board declassification proposals and six director resignation proposals – and compensation (3%) made up nearly half of tech-sector proposals, compared to 46% and 9%, respectively, for 2024. Among tech companies, governance proposals also received the highest level of support at 39.1%, a slight increase from 36% in the prior year. Compensation proposals saw support increasing to 30.4% from 10%, though the sample size was relatively small (three compensation proposals in 2025, compared to 14 in 2024).

The percentage of governance and compensation proposals in the tech sector was slightly higher than in the Russell 3000 (45%), largely a function of the relatively low number of environmental proposals for tech sector companies, which remained flat in 2025 at 10%. Environmental proposals continued to receive only moderate support as well, decreasing from 20% in 2024 to 12% in 2025. The number of social proposals increased from 33% of all proposals in 2024 to 45% in 2025, and average support for social proposals slightly declined, from 15% to 12% in the same period. Top 2025 social proposals included viewpoint discrimination proposals from anti-ESG proponents (13, 17% of social proposals) and traditional human rights (five, 7%), diversity and pay gap matters (nine, 12%), AI policies (eight, 11%) and online child safety (five, 7%).

Life sciences proposals by market cap

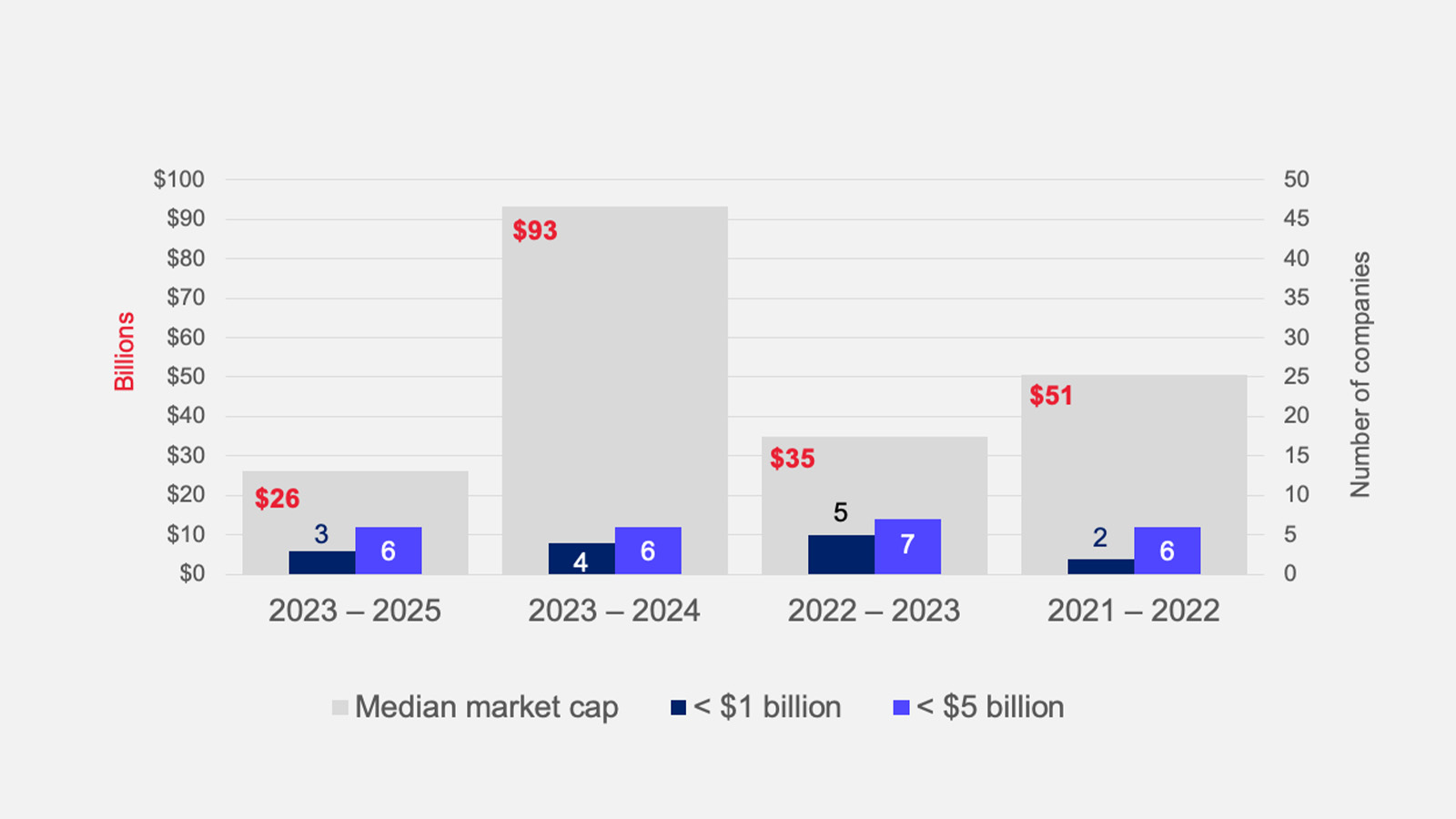

Overall trends in the life sciences4 sector are broadly consistent with the tech sector. Proposals are heavily concentrated among large-cap issuers, with 2025 witnessing an increase in the median market cap of proposal recipients, rising to $98 billion from $93 billion in 2024, $35 billion in 2023 and $51 billion in 2022. A limited number of smaller-cap companies continue to receive proposals, with six companies under $5 billion (three under $1 billion) receiving proposals in 2025, compared to six in 2024 and seven in 2023 (five under $1 billion) and six in 2022 (two under $1 billion).

Life sciences proposals by category

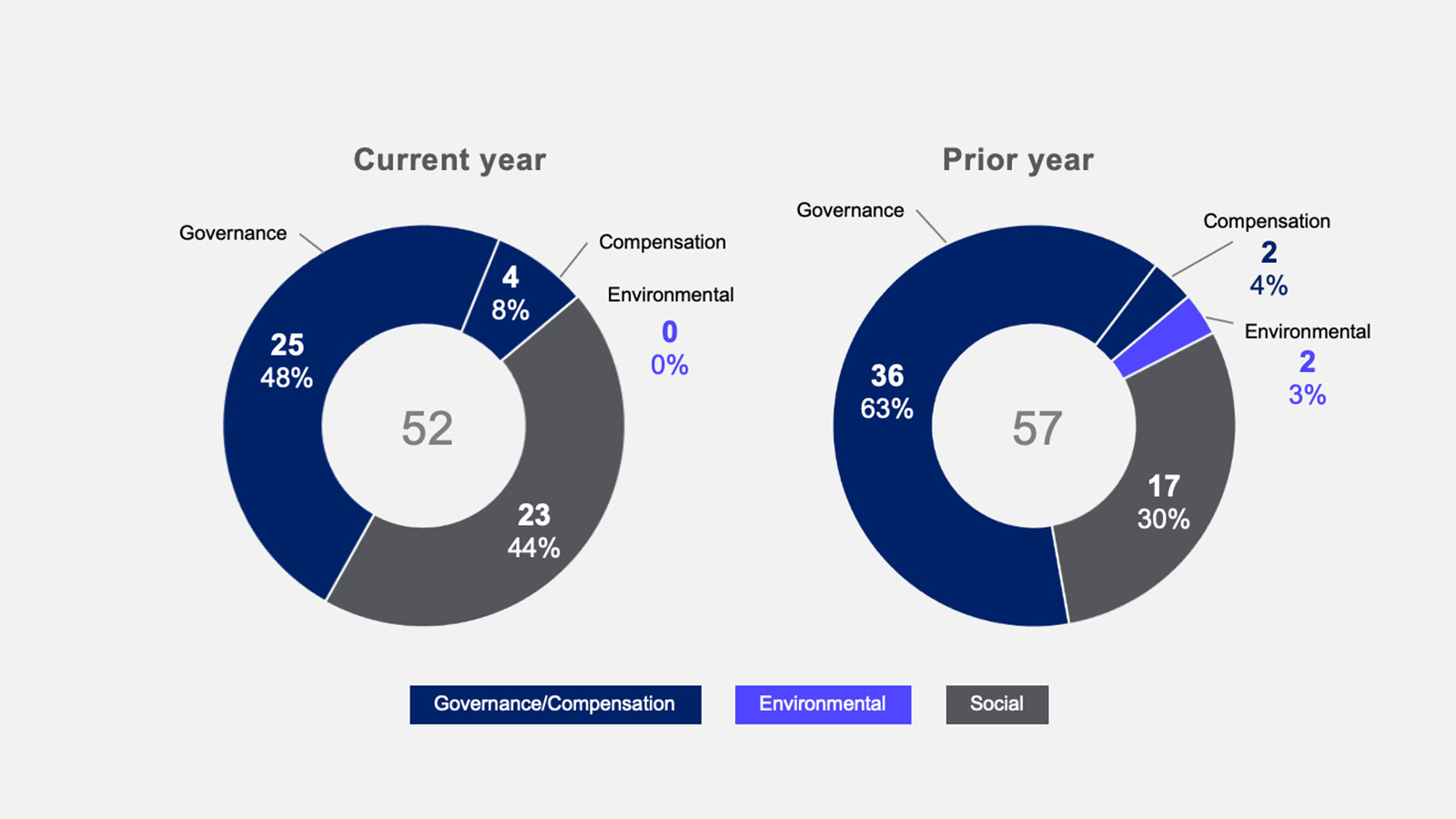

Life sciences companies received approximately 70% fewer proposals than tech companies, with only 52 proposals in the 2025 season, a 9% decline from the prior year. Even more than in the tech sector, proposals were dominated by governance and compensation – together making up 56% of all life sciences proposals, particularly traditional governance proposals, where average support held steady, from 38% to 38.5%. Social proposals increased from 30% to 44%, with average support falling from 13% to 10%. Consistent with previous years, social proposals included a broad mix of generally applicable topics, such as human rights and racial equity audits, and industry-specific topics, particularly, patient access and intellectual property issues. Notably, in 2025, there were no environmental proposals at life sciences companies, and compensation proposals remained in the low single digits.

Management proposals

Director elections

Director Election Vote Results by Support Level

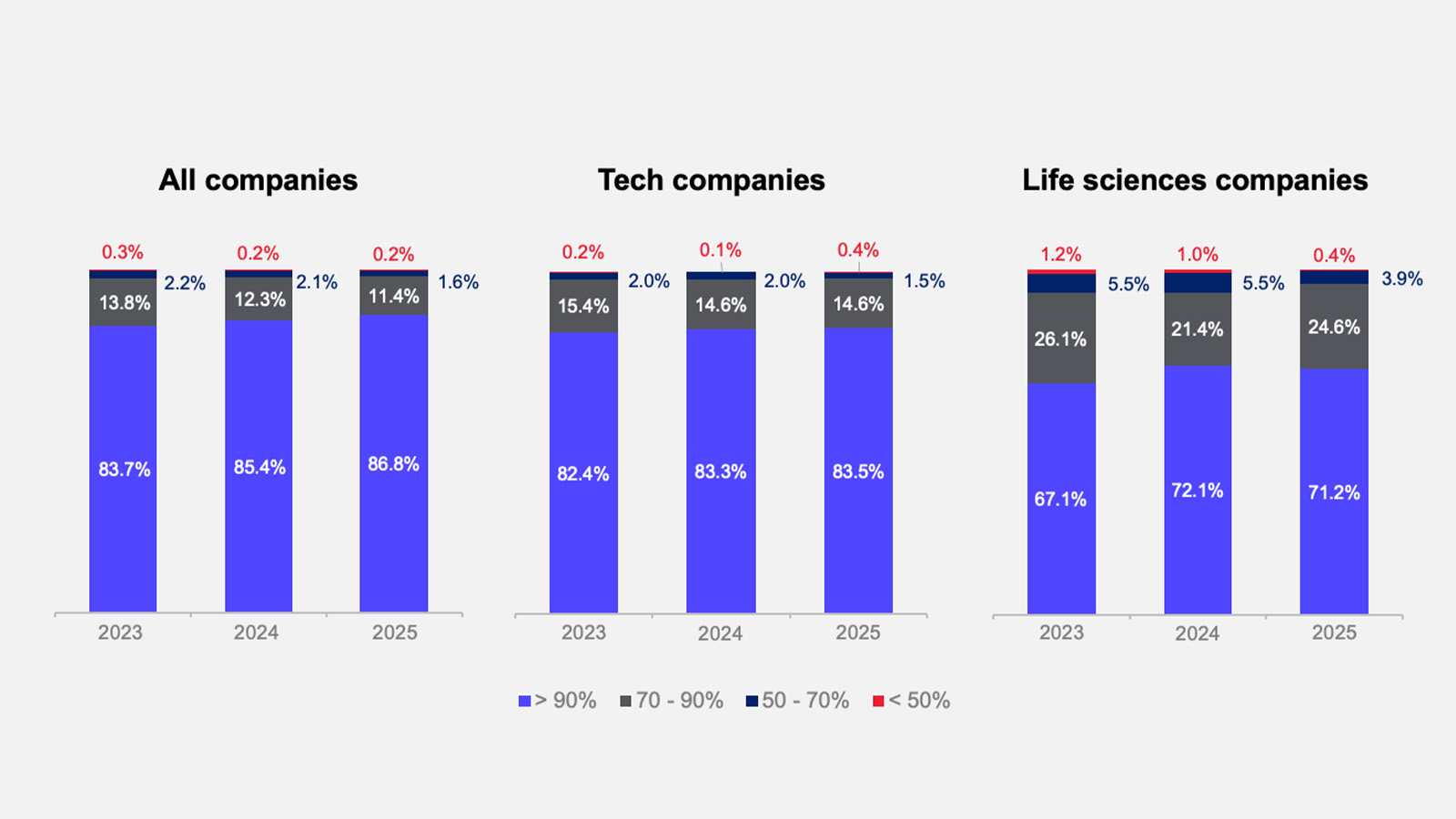

Director election outcomes improved across multiple dimensions in the 2025 proxy season. Average support for director nominees across the Russell 3000 index rose to 95.1%, continuing an upward trend from 94.8% in 2024 and 94.4% in 2023. At the same time, the proportion of directors receiving less than 70% support – a key indicator of significant shareholder dissatisfaction – declined meaningfully to 1.9%, down from 2.3% in 2024 and 2.5% in 2023. Strong support levels also became more widespread, with 86.8% of directors receiving more than 90% support, a notable increase from 85.4% in 2024 and 83.7% in 2023.

Impact of ISS Opposition on Director Elections

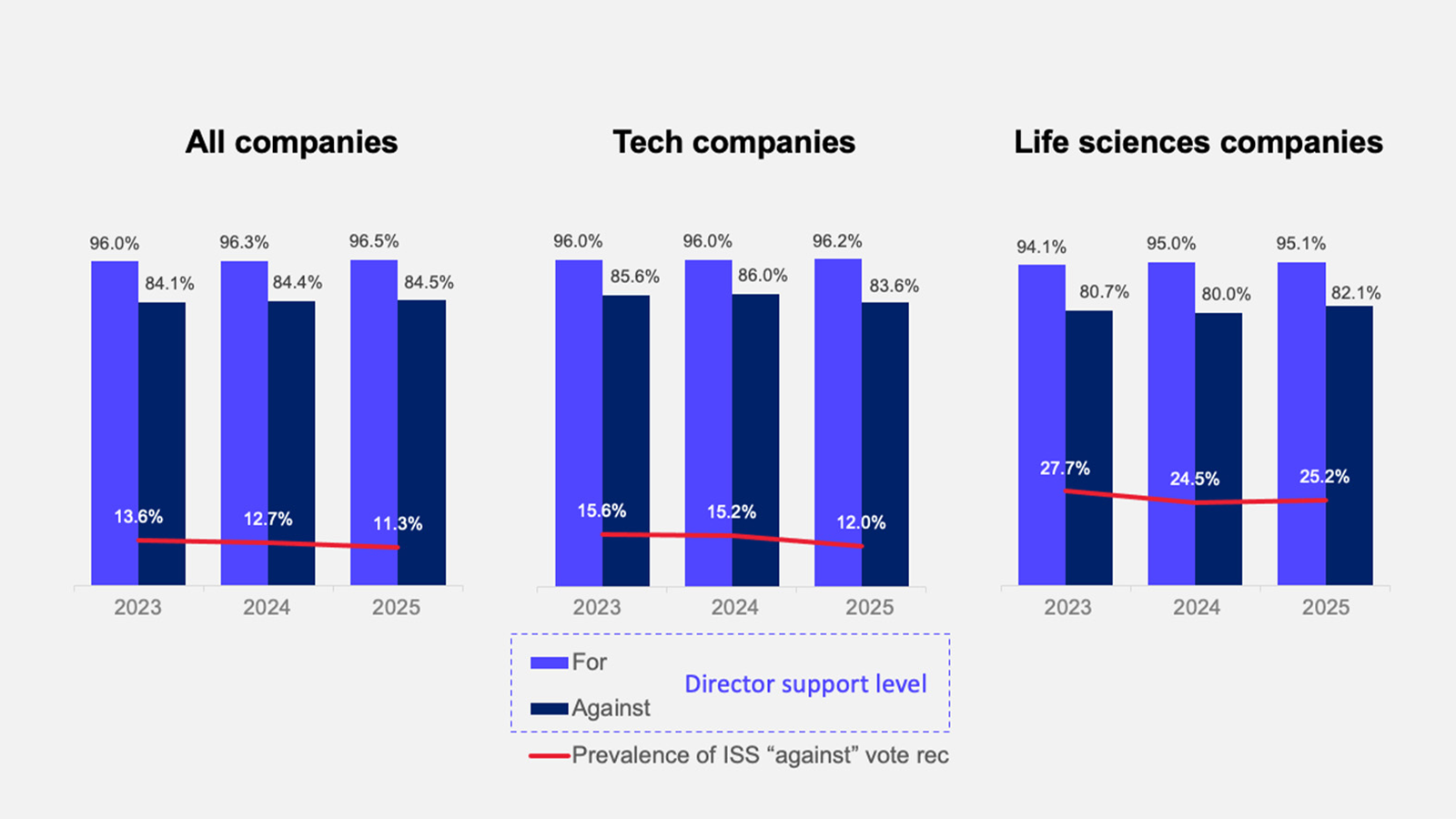

Institutional Shareholder Services (ISS) issued fewer adverse recommendations again this proxy season, opposing just 11.3% of director nominees, down from 12.7% in 2024 and 13.6% in 2023. Despite this reduced opposition, ISS’s influence remained stable. Directors receiving ISS support averaged 96.5% support, while those facing ISS opposition averaged 84.5%, sustaining the roughly 12-point gap seen in recent years.

Tech and life sciences companies experienced similar gains in director election outcomes, though shareholder scrutiny and proxy advisor opposition remained elevated relative to the broader index. Average support for director nominees climbed to 94.6% at tech companies (up from 94.5% in 2024 and 94.3% in 2023) and to 91.8% at life sciences companies (up from 91.3% in 2024 and 90.4% in 2023). The percentage of directors receiving under 70% support also declined in both sectors, falling to 1.9% at tech companies (from 2.2% in both 2024 and 2023) and to 4.2% at life sciences companies (from 6.5% in 2024 and 6.8% in 2023).

Despite these improvements, ISS continued to oppose director nominees at elevated rates in the tech and life sciences sectors. In the tech sector, 12% of nominees faced ISS opposition – an improvement from 15.2% in 2024 and 15.6% in 2023 – while 25.2% of life sciences nominees were opposed, largely consistent with historical levels. The influence of these recommendations varied between the two sectors. The impact appeared to ease in the life sciences sector, where the gap in average support between ISS-supported and ISS-opposed nominees narrowed to 13% (down from 14.9% in 2024 and 13.4% in 2023), but intensified in the tech sector, where the gap widened to 12.6% (up from 10% in 2024 and 10.4% in 2023), indicating increased sensitivity to proxy advisor guidance among tech investors this season.

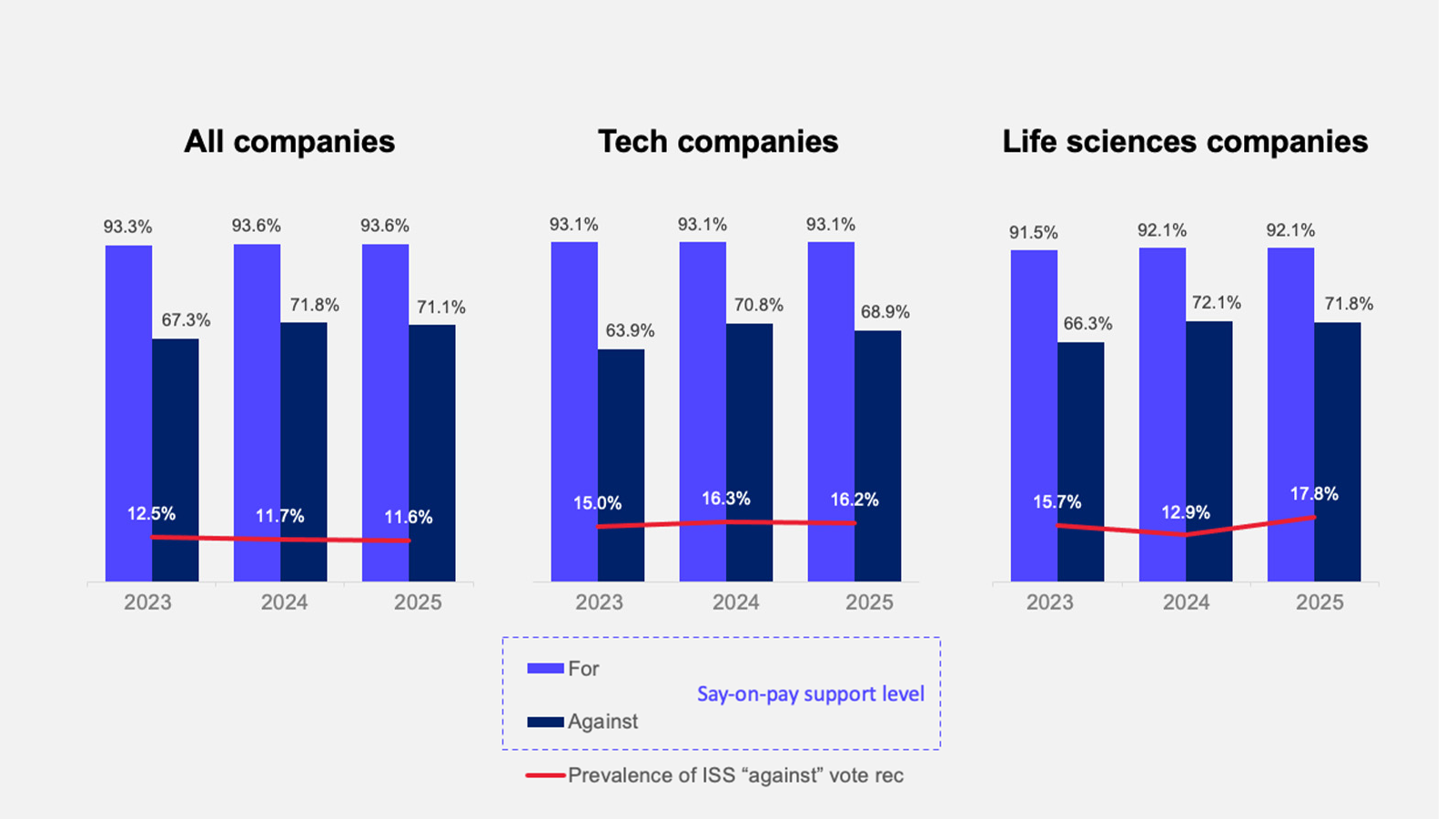

Say on pay

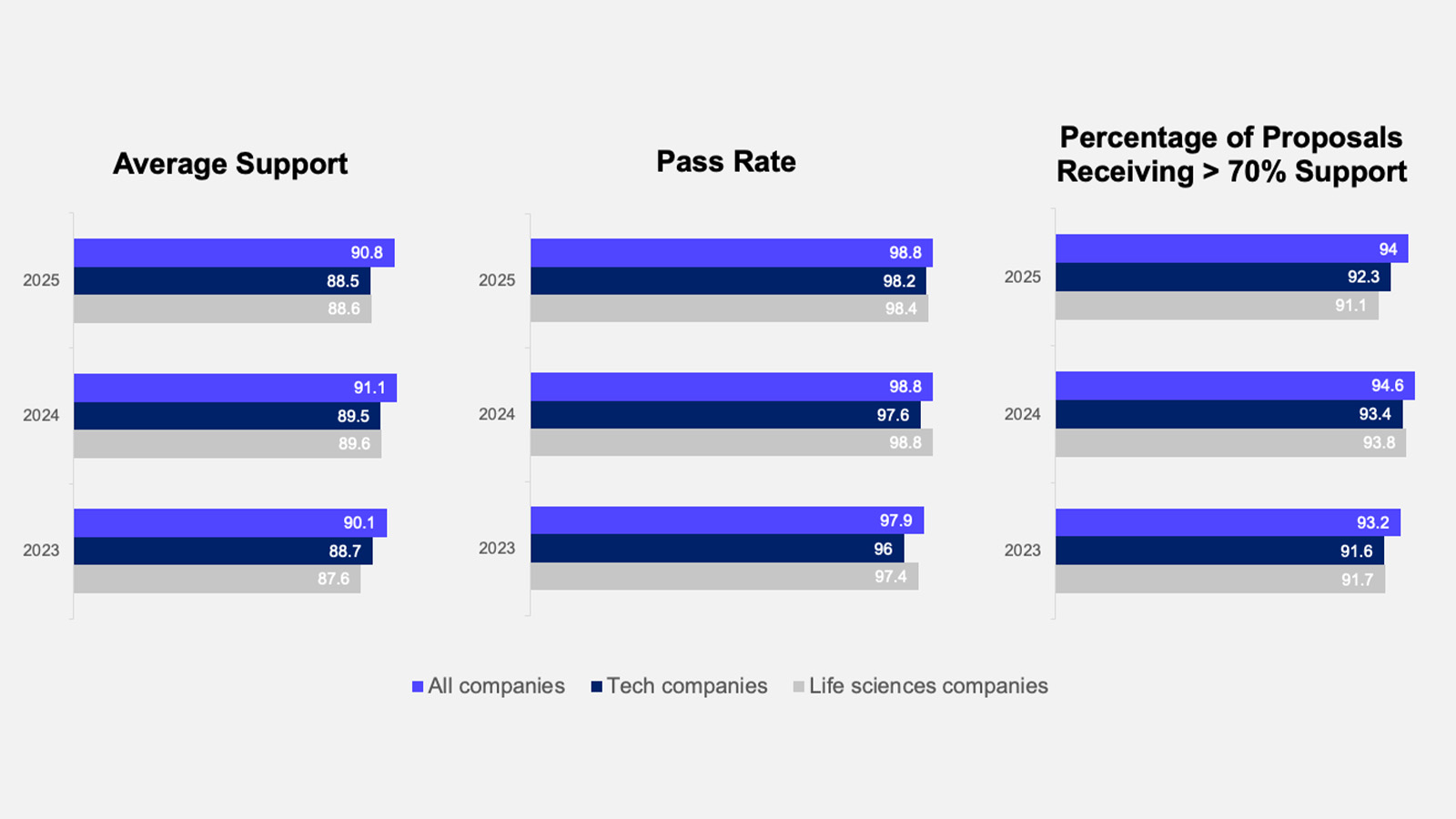

Shareholder support for say-on-pay proposals remained robust across the Russell 3000 index in the 2025 proxy season. A total of 98.8% of companies secured majority support, consistent with 2024 and up from 97.9% in 2023, and average support came in at 90.8%, slightly below last season’s 91.1% but ahead of the 2023 season’s 90.1%. Additionally, 94% of companies received more than 70% support, sustaining historically elevated levels following 94.6% support last season.

Impact of ISS Opposition on Say-on-Pay

ISS recommendations continued to play a meaningful role in shaping say-on-pay proposal outcomes. While the percentage of proposals receiving an ISS “against” recommendation declined slightly to 11.6% – down from 11.7% in 2024 and 12.5% in 2023 – the influence of those recommendations appeared to solidify. Companies that received ISS support averaged 93.6% shareholder approval, compared to 71.1% for those opposed, resulting in a 22.5-point gap. This gap represents a slight increase from the 21.8-point gap observed in 2024, but is still down from the 26.1-point gap seen in 2023, reflecting a modest rebound in the impact of proxy advisor guidance on say-on-pay outcomes following a notable dip last year.

Tech and life sciences companies continued to receive strong, though comparatively lower, say-on-pay support than the broader index. Tech companies saw a 98.2% pass rate in 2025 (up from 97.6% in 2024 and 96% in 2023), with 92.3% receiving more than 70% support, and average support was 88.5% (down from 89.5% in 2024 and 88.7% in 2023). Life sciences companies also saw solid results, with a 98.4% pass rate (down from 98.8% in 2024 but up from 97.4% in 2023), 91.1% clearing the 70% support threshold, and average support of 88.6% (down from 89.6% in 2024 but up from 87.6% in 2023).

Both tech and life sciences companies continued to face higher rates of ISS opposition on say-on-pay proposals compared to the broader index. This season, 16.2% of tech companies and 17.8% of life sciences companies received ISS “against” recommendations on their say-on-pay proposals – compared to just 11.6% across the Russell 3000 index. While ISS’s opposition to tech companies’ say-on-pay proposals was roughly in line with historical levels, life sciences companies saw a notable increase from the 12.9% opposition rate observed in 2024. The impact of these recommendations also varied, as the gap in support between ISS-backed and ISS-opposed proposals held relatively steady at 20.4 points for life sciences companies (compared to 20 points in 2024) but expanded to 24.3 points for tech companies from 22.4% – suggesting (once again) heightened investor responsiveness to proxy advisor guidance in the tech sector this season.

Importantly, strong say-on-pay support in one year does not ensure continued shareholder support in the next. Among companies that failed their say-on-pay proposal in 2025, average support in the prior year was a solid 88.2%, underscoring how quickly sentiment can shift in response to evolving pay practices, performance outcomes or other governance concerns. Meanwhile, most companies that failed in 2024 saw support rebound in 2025, though generally only modestly – average support among these companies was 74.6% – indicating that regaining shareholder trust can be a gradual process, even when changes are made.

Equity compensation plan proposals

Shareholders continued to support equity compensation plan proposals at high levels in the 2025 proxy season. The pass rate rose to 99.4%, up from 99.1% in 2024 and 98.9% in 2023, and average support held steady at 87.4%. While ISS opposed a larger share of proposals this season (32.8%, up from 30.3% in 2024 and 30.7% in 2023), its influence appeared to moderate slightly. The gap in average support between ISS-supported proposals (93%) and ISS-opposed proposals (75.9%) narrowed to 17.1 points, down from 17.8 points last year, suggesting investors may have weighed equity plans more independently this season despite increased proxy advisor opposition.

Sector-specific dynamics revealed continued pressure in the tech and life sciences sectors. ISS opposed 57% of life sciences companies’ equity plan proposals – far above the 32.8% rate observed for the broader index – likely contributing to lower average support of 81.4%. Still, all life sciences proposals passed, pointing to investor recognition of the sector’s unique capital demands and extended development cycles, which may justify more flexible equity strategies. In the tech sector, all but one proposal passed, with average support of 85.1%, and though the rate of ISS opposition was consistent with the broader index at 34.8%, the impact of that opposition was more meaningful: the gap between ISS-supported proposals and ISS-opposed proposals widened to 21.2 points for tech companies – markedly above the 17.1-point gap observed for the broader index and the 15.3-point gap seen for life sciences companies. This widening gap may point to heightened responsiveness among investors to ISS concerns around dilution, plan cost or plan design features in the tech sector.

Officer exculpation proposals (Delaware-incorporated companies only)

Following amendments to the Delaware General Corporation Law in August 2022, Delaware corporations are now permitted to adopt charter provisions limiting certain officers’ personal liability for monetary damages arising from breaches of the fiduciary duty of care, protections previously available only to directors. In response, many companies have sought shareholder approval to adopt such officer exculpation provisions through charter amendments, which typically require approval by at least a majority of outstanding shares. To date, 90% of these proposals have passed, with average support of 71.5%, indicating generally favorable – though not overwhelming – investor support when measured against the more demanding voting threshold.

Officer exculpation proposals have received varying levels of shareholder support in the tech and life sciences sectors. Tech companies have generally tracked with the broader Russell 3000, achieving an 89.1% pass rate and 70.8% average support. However, life sciences companies have continued to face steeper challenges. Despite receiving ISS support for 96.8% of proposals – well above the support levels observed for tech companies (78.3%) and the broader index (84.1%) – only 81.7% of life sciences company proposals have passed, with average support at just 66.6%.

The comparatively lower support for officer exculpation proposals at life sciences companies appears to be driven more by structural voting challenges than by investor opposition. These companies often have a higher proportion of retail investors, who typically participate in proxy voting at lower rates than institutional shareholders. As a result, securing the majority (or supermajority) of outstanding shares needed to approve charter amendments can be more difficult. Notably, when support is measured based on votes cast, life sciences companies outpace both tech companies and the broader index – achieving 91.5% average support, compared to 88.6% and 89.3%, respectively. This dynamic suggests that turnout, rather than investor sentiment, may be the key factor limiting approval rates in the sector.

Responsive governance proposals

In 2025, Russell 3000 companies continued to put up high volumes of management proposals requesting shareholder approval of corporate governance charter provisions. Such proposals are generally responsive to shareholder pressure, particularly prior-year passing proposals or the same-year submission of proposals with high historical passage rates (e.g., board declassification). While shareholder support for many proposal topics ebbs and flows, these management proposals highlight consistent shareholder support for governance proposals related to a limited number of core “good governance” topics. While these proposals generally receive almost universal support from voting shareholders, passage rates are consistently lower due to the effects of charter amendment standards requiring approval of a majority (or supermajority) of outstanding shares, rather than votes cast.

Following the high success levels for simple majority shareholder proposals in 2024 (30 passing proposals), management proposals requesting the approval of charter amendments removing supermajority provisions were submitted in high levels in 2025, 76 compared to 44in 2024.

Management proposals requesting approval of the declassification of boards of directors also were submitted in high numbers in 2025 – 54 compared to 40 in 2024 – which followed six passing declassification shareholder proposals in the 2024 season and none in 2023. Given the extremely high passage rate of declassification shareholder proposals, many companies put up management proposals in response to informal shareholder pressure or as a negotiated concession for the withdrawal of a shareholder proposal.

Twenty-seven management proposals in 2025 related to the creation or expansion of shareholder special meeting rights (compared to 20 in 2024), the only other corporate governance amendment management proposal submitted in significant numbers, following seven passing shareholder proposals in 2024 and five in 2023.

Notes

- The data presented in this alert is sourced from ISS’s voting analytics, as well as other databases, information publicized by shareholder proposal proponents and companies, and independent research, and focuses exclusively on companies in the Russell 3000 index.

- For purposes of shareholder proposals discussed in this alert, “tech” includes core hardware, software and computing companies, as well as web-focused businesses in retail, transportation, business services and other industries, such as ride share, ecommerce and fintech companies, in an attempt to approximate lay perceptions. Due to the volume of management proposals, discussion of management proposals in this alert involves a more restrictive definition of tech, focusing on companies classified under Global Industry Classification Standard (GICS) codes 4510 (Software & Services), 4520 (Technology Hardware & Equipment) and 4530 (Semiconductors & Semiconductor Equipment).

- For purposes of shareholder proposals discussed in this alert, “tech” does not include the 13 shareholder proposals submitted to one mega-cap company due to its meeting falling outside the July 1, 2024 – June 30, 2025, date range.

- For purposes of all proposals discussed in this alert, “life sciences” refers to companies classified under GICS code 3520 (Pharmaceuticals, Biotechnology & Life Sciences).

Related Contacts

This content is provided for general informational purposes only, and your access or use of the content does not create an attorney-client relationship between you or your organization and Cooley LLP, Cooley (UK) LLP, or any other affiliated practice or entity (collectively referred to as "Cooley"). By accessing this content, you agree that the information provided does not constitute legal or other professional advice. This content is not a substitute for obtaining legal advice from a qualified attorney licensed in your jurisdiction, and you should not act or refrain from acting based on this content. This content may be changed without notice. It is not guaranteed to be complete, correct or up to date, and it may not reflect the most current legal developments. Prior results do not guarantee a similar outcome. Do not send any confidential information to Cooley, as we do not have any duty to keep any information you provide to us confidential. When advising companies, our attorney-client relationship is with the company, not with any individual. This content may have been generated with the assistance of artificial intelligence (Al) in accordance with our Al Principles, may be considered Attorney Advertising and is subject to our legal notices.