2026 Shareholder Proposal Season Early Review and Look Ahead to 2027

’Cause when life looks like Easy Street, there is danger at your door

Despite the heightened drama of the 2026 shareholder proposal season – precipitated by the landmark announcement from the staff of the Division of Corporation Finance of the SEC (SEC staff) that it would generally not respond to no-action requests during the 2026 proxy season – the year-over-year trends remained largely consistent with the prior year. Overall proposal volume continued to decline, driven primarily by fewer environmental and social (E&S) proposals, while governance and anti-ESG proposal activity and support levels remained broadly consistent with last year.

This alert provides an overview of proposal submissions and early voting trends for the 2026 season, examines exclusion and litigation developments under the SEC staff’s new no-action policy, as well as evolving proponent tactics, and considers the implications for what may be an even more chaotic 2027 season.

Key takeaways so far:

- Overall submission and voting trends in 2026 are consistent with 2025: Aggregate proposal volumes continue to decline, driven primarily by fewer E&S proposals, which continue to attract low shareholder support, while governance proposals remain steady with continued robust support.

- The SEC staff’s effective withdrawal from the Rule 14a-8 no-action process introduced significant uncertainty in 2026, contributing to a likely increase in negotiated withdrawals and a marked reduction in companies submitting unilateral Rule 14a-8(j) exclusion notices relative to prior-year no-action requests.

- A significant uptick in proponent litigation in 2026 may introduce a disruptive dynamic into the 2027 season, further complicating how companies navigate shareholder proposal management.

- The prospect of an SEC rulemaking to substantially revise or rescind Rule 14a-8 altogether may shape proponent strategies in 2027, though any such rule change would almost certainly face substantial legal and procedural challenges and would likely not take effect before the next proxy season.

- Shareholder proponents and activists have continued to deploy innovative strategies in 2026, which may preview the pressure tactics companies can expect in 2027 or following a potential Rule 14a-8 rescission.

Recap of SEC actions

In September 2025, SEC Chairman Paul Atkins indicated that the SEC staff would explore ways to give companies additional tools to challenge shareholder proposals. In that speech, Atkins suggested the SEC staff might take a favorable view of companies submitting Delaware law opinions asserting that precatory proposals are improper under state law or adopting bylaw amendments that impose submission requirements beyond those in Rule 14a-8. Atkins also signaled the SEC was considering a comprehensive reassessment of Rule 14a-8’s role and purpose. Although amendments to Rule 14a-8 are on the SEC’s current rulemaking agenda, the SEC has not yet advanced a rule proposal.

In November 2025, the SEC staff announced a new policy for the 2026 proxy season under which it would no longer provide substantive responses to Rule 14a-8 no-action requests from companies seeking to exclude shareholder proposals from their definitive proxy materials, except for requests based on Rule 14a-8(i)(1) state law violation arguments. Companies seeking to exclude a shareholder proposal must still submit a notice of intent to exclude the proposal under Rule 14a-8(j). While the policy may have been intended to encourage companies to pursue the types of Delaware state law violation arguments under Rule 14a-8(i)(1) contemplated by Atkins, no companies have done so to date.

Initial expectations that the policy would lead to widespread unilateral exclusions and greater proponent flexibility in negotiating withdrawals have not fully materialized. As discussed below, a significant number of companies chose to exclude proposals, and the uncertainty generated by the SEC staff’s current no-action policy appears to have influenced some negotiations. However, the percentage of proposals included in proxies remained generally consistent with prior years, and in some proposal categories (social and anti-ESG proponent proposals) increased. In addition, the emergence of proponent-initiated litigation in March may further complicate the landscape if the SEC staff, as expected, maintains its current no-action policy for the 2027 season.

Notably, anticipated proxy advisor opposition to companies that unilaterally excluded shareholder proposals this season did not materialize, notwithstanding policy statements issued by Institutional Shareholder Services (ISS) and Glass Lewis indicating they would scrutinize companies’ Rule 14a-8(j) exclusion notices. Adverse vote recommendations on that basis were virtually nonexistent, with proxy advisors generally deferring to companies’ judgments where companies provided substantive explanations in support of the exclusion. Should proxy advisors adopt a more aggressive approach for the 2027 proxy season, companies would need to incorporate the prospect of proxy advisor opposition into their shareholder proposal exclusion analysis.

Proposal submissions and early vote results

The analysis below reflects shareholder proposals submitted for annual shareholder meetings at Russell 3000 companies scheduled between January 1 and June 30, 2026 (the 2026 proxy season). This alert adopts a January 1 through June 30 measurement period for all years referenced in the analysis – a departure from prior-year alerts, which used a July 1 through June 30 period – to align with the SEC staff’s announcement of its no-action policy for the 2026 season.[1] Vote results capture outcomes through May 25, leaving 131 proposals, approximately 32% of all proposals appearing in proxy statements to date, to be voted on this season. As a result, the voting trends discussed herein are preliminary and will continue to evolve as additional meetings are held.

Overview

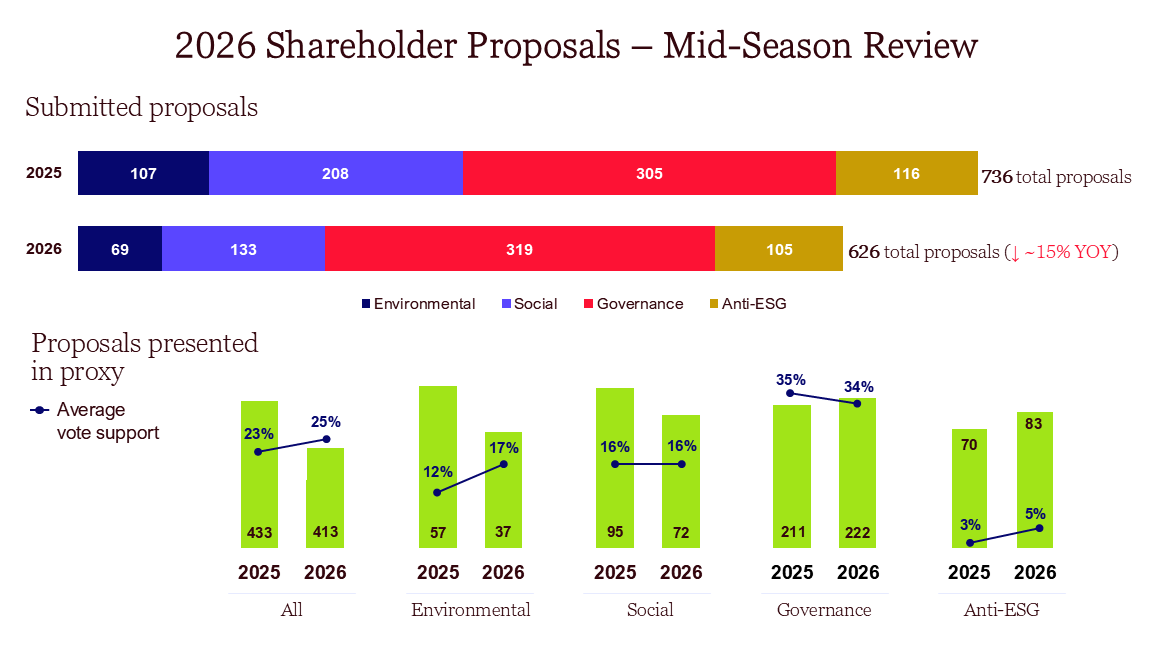

The 2026 proxy season reflects a continuation of several multiyear trends, including a steep and sustained decline in E&S proposal submissions, steady governance proposal volume and a growing share of submissions from anti-ESG proponents. Of the 626 proposals submitted this season, approximately 66% have appeared in proxy statements, generally consistent with recent years (59% in 2025 and 63% in 2024). Average support across all proposal categories has risen slightly to 24.6% in 2026, up from 22.7% in 2025 and 22.5% in 2024.

A notable development this season is the sharp increase in ISS support rates. After recommending in favor of only 34.1% of proposals in 2025, ISS has supported 47.9% of proposals to date this season, broadly in line with its 47.3% support rate in 2024. That shift is reflected across all proposal categories, most strikingly for environmental proposals, where ISS support jumped from 0% in 2025 to 16.7% in 2026. The return of ISS support is likely a contributing factor to the modest improvement in average vote outcomes this season.

Anti-ESG proponents submitted 105 proposals in 2026, consistent with recent years, and average support for those proposals edged up to 5.3% from approximately 2.5% in each of the prior two years, principally driven by higher investor support for independent board chair proposals from those proponents.

Governance proposals

Governance proposals remained steady in volume and continue to receive relatively robust support. Proponents submitted 319 governance proposals in 2026, compared to 305 in 2025 and 316 in 2024, and average support of 33.8% is only slightly below the 35.2% and 35.1% averages observed in 2025 and 2024, respectively. As in prior seasons, governance proposal submissions were heavily concentrated among a small group of serial proponents, who collectively accounted for more than 75% of this season’s submissions.

Several governance proposal topics stand out this season:

- Independent board chair – Submissions surged to 99 submissions in 2026 from just 31 in 2025, with average support of 24.6% (down from 31.3% in 2025).

- Shareholder written consent rights – Submissions increased sharply to 51 submissions in 2026 from 11 in 2025, all from the same group of proponents referenced above, and average support increased to 38.3% (from 26.3% in 2025).

- Shareholder special meeting rights – This remained a prominent proposal topic in 2026, with 59 submissions (down from 70 in 2025), and average support of 39.2% (up from 32.8% in 2025).

- Simple majority voting – Proposals to eliminate supermajority voting provisions from governing documents declined to 32 submissions in 2026 from 40 in 2025, but remain among the highest-supported proposal topics at 59.1% average support, albeit down from 71.9% in 2025.

The following governance proposal topics have achieved majority support in 2026 to date:

- Elimination of supermajority voting provisions from governing documents (5 proposals)

- Establishment of shareholder special meeting rights (4)

- Establishment of shareholder written consent rights (3)

- Board declassification (3)

- Shareholder approval prior to issuance of blank check preferred shares (2)

- Adoption of a majority vote standard for director removal (1)

- Shareholder approval of certain change-in-control severance agreements (1)

Notably, Exxon Mobil Corporation received a proposal this season relating to its new retail voting program, launched in September 2025, which allows retail holders to opt in to provide standing instructions to vote their shares at all future meetings in line with the board’s recommendations. The proposal requested that the company modify the program to offer additional voting options not aligned with the board’s recommendations. It failed with 23.5% support, but litigation challenging Exxon’s program remains ongoing.

Social proposals

Social proposal submissions continued their sharp multiyear decline. Proponents submitted 133 social proposals in 2026, down from 208 in 2025 and 298 in 2024, while average support has modestly increased to 16.4% (from 16% in 2025, though it has fallen from 19.6% in 2024).

The decline in lobbying proposals was particularly pronounced, falling from 38 submissions in 2025 to just seven in 2026. This drop likely reflects both successful exclusions in 2024 and 2025 on Rule 14a-8(i)(7) grounds and the low support these proposals received in 2025 (13.3%), though average support has rebounded to 26.5% this season. By contrast, political contributions proposals increased to 29 submissions (from 18 in 2025), likely buoyed by strong support last year (40.9%), though support has moderated to 28.2% this season.

Diversity proposals also continued their multiyear decline, falling to 19 submissions from 44 in 2025 and 68 in 2024. Average support declined to 13.6%, down from 14.3% in 2025 and 21.7% in 2024.

AI proposals attracted renewed attention in 2026. After first emerging in 2024, proponents submitted 14 AI-related proposals this season, compared to eight in 2025 and 11 in 2024. To date, only two AI-related proposals have been voted on, both submitted by anti-ESG proponents, and they received average support of 5.3%.

No social proposals have received majority support to date this season, but several topics have garnered more than 25% support:

- Political contributions (6 proposals)

- Lobbying payments (1)

- Collective bargaining rights (1)

Environmental proposals

Environmental proposal submissions also continued their pronounced decline, falling to 69 proposals in 2026 from 107 in 2025 and 163 in 2024. Despite this reduced volume, average support for environmental proposals has increased moderately to 17% in 2026 from 12.4% in 2025 – a shift that correlates with the reversal in ISS recommendations this season.

Proposals focused on emissions-related reporting reflect the broader trend, declining from 42 submissions in 2025 to 22 in 2026, while average support is up to 22.9% from 12.9% in 2025 (though still below the 26.6% average in 2024). Among environmental proposals, emissions-related reporting is the only topic to receive greater than 25% support to date this season (3 proposals).

Impact of withdrawn proposals

Shareholder proposal data is subject to inherent uncertainty each year due to the impact of nonpublic proposal withdrawals. While withdrawals following a Rule 14a-8(j) exclusion notice or proxy filing, as well as those publicized by proponents, are reflected in the data, many companies and proponents negotiate withdrawals privately and before any filings or other proponent disclosures occur. The uncertainty created by the SEC staff’s current no-action policy appears to have increased the incentive for such negotiations in 2026, and our experience suggests that withdrawal volumes were likely higher this season than in prior years.

As discussed in our 2025 proxy season alert, the mid-season publication of Staff Legal Bulletin No. 14M in February 2025, which rescinded perceived proponent-friendly guidance published in 2021 that had limited companies’ ability to exclude proposals raising issues with “broad societal impact,” may also have contributed to elevated withdrawal activity last year. As a result, the year-over-year declines in submitted proposals between 2026 and 2025, and between 2025 and earlier years, may be meaningfully overstated due to the likelihood that a significant number of negotiated withdrawals were not publicized.

Proposal exclusions and litigation

As of June 1, companies had submitted 170 Rule 14a-8(j) exclusion notices under the SEC staff’s current no-action policy since its announcement in November 2025, compared to 360 no-action requests submitted during the comparable period of the prior season (November 2024 through May 2025). Even accounting for the year-over-year decline in proposal submissions, the magnitude of this decrease – a 53% reduction in exclusion-related filings against a 15% reduction in proposal submissions – suggests that a meaningful number of companies that would have sought no-action relief in prior years elected not to pursue exclusion under the SEC staff’s revised approach.

Companies’ decisions appear to have reflected a probability/magnitude assessment of the risks associated with unilateral exclusion. For many companies, even a relatively low probability of costly shareholder litigation (along with the negative publicity such litigation can generate), together with the prospect of adverse proxy advisor recommendations against individual directors, was sufficient to outweigh the benefits of exclusion, given the severity of those potential consequences. While anticipated proxy advisor opposition largely failed to materialize, litigation challenging proposal exclusions emerged later in the season, as discussed below.

The 170 Rule 14a-8(j) exclusion notices submitted this season included a mix of substantive and procedural exclusion bases, as reflected below. Notably, however, companies relied considerably less on certain substantive arguments requiring more subjective judgments. This trend was particularly evident for ordinary business and micromanagement exclusions under Rule 14a-8(i)(7), which appeared in only 33% of Rule 14a-8(j) exclusion notices this season, down markedly from the 56% rate observed in 2025 no-action requests. This may reflect a broader inclination among companies to adopt a more conservative posture under the SEC staff’s current no-action policy, favoring more objective bases for exclusion. This season’s Rule 14a-8(j) exclusion notices included:

- 51 exclusions based purely on procedural grounds

- 51 exclusions citing Rule 14a-8(i)(7) (ordinary business/micromanagement)

- 34 exclusions citing Rule 14a-8(i)(10) (substantial implementation)

- 17 exclusions citing Rule 14a-8(i)(3) (false/misleading)

Following the SEC staff’s announcement of its no-action policy for the 2026 season, early commentary focused on the potential for proponent litigation in the absence of the SEC staff’s role as arbiter, and the possibility that this risk would drive conservative company approaches to unilateral exclusions under the new policy. Early Rule 14a-8(j) exclusion notices appeared to confirm this expectation, emphasizing procedural and relatively straightforward substantive bases. Beginning in February, however, companies increasingly asserted 14a-8(i)(7) and other more expansive exclusions, suggesting an increase in company confidence. That trend shifted again in late February, when the first of what are now six proponent lawsuits was filed challenging the validity of company exclusions under Rule 14a-8.

Of the six lawsuits filed to date, one covered a human rights and diversity proposal, four covered E&S proposals, and one covered a political spending and lobbying proposal. In five of the six cases, the company relied on the “ordinary business” exclusion under Rule 14a-8(i)(7); the sixth was based on procedural defects.

As of June 2, 2026, three lawsuits have been settled, with companies agreeing either to implement the proposal or include it in their proxy materials. One case was voluntarily dismissed, and two remain pending. In the pending matters, one company filed its 2026 proxy statement with the proposal included after the court denied the company’s motion to dismiss and granted the proponent’s motion for injunctive relief, while the other filed the proxy without the proposal after the court denied the proponent’s motion for a preliminary injunction.

An even earlier look at 2027

Prospects for Rule 14a-8 repeal

The SEC’s 2026 rulemaking agenda includes a potential proposal addressing Rule 14a-8, and many observers have speculated that the SEC may seek to rescind the rule entirely. Any such proposal would be subject to the SEC’s standard rulemaking process, including notice-and-comment procedures. Given Rule 14a-8’s central role in the shareholder proposal landscape, a rescission proposal would likely generate a substantial volume of public comments (e.g., investor groups are already petitioning to keep Rule 14a-8 in place), requiring meaningful consideration by the SEC before adoption of a final rule. Recent SEC rulemakings have frequently taken more than a year to progress from proposal to adoption, suggesting that one or more proxy seasons could continue under the SEC staff’s current no-action policy before any rescission could become effective. In addition, a rescission of Rule 14a-8 would almost certainly face legal challenges, which could result in injunctive relief or a voluntary SEC stay (as occurred with the SEC’s 2024 climate rules). Consequently, uncertainty surrounding the future of Rule 14a-8 could persist past the 2028 presidential election.

2027 shareholder proposal landscape

Regardless of the timing of any SEC rulemaking, the prospect of a Rule 14a-8 rescission is likely to influence the 2027 proxy season. An imminent or pending rescission proposal may create a highly contentious “last chance” environment in which proponents seek to maximize leverage while the SEC staff’s current no-action policy remains in effect. One potential consequence may be proponents submitting precatory or binding bylaw proposals designed to provide shareholders with proposal access rights independent of Rule 14a-8.

The 2027 season could be further complicated if the SEC staff maintains its current no-action policy. Under that scenario, companies may have reduced leverage in negotiations with proponents, particularly given proponents’ demonstrated willingness during the 2026 season to use litigation as a means of challenging proposal exclusions.

Faced with elevated proposal volumes and heightened litigation risk, some companies may conclude in 2027 that allowing a greater number of proposals to proceed to a vote presents the lower-risk path, particularly on E&S topics, where shareholder and proxy advisor support continues to erode. That calculus may differ, however, for proposals addressing more consequential matters, such as binding bylaw amendments, or proposals with a greater likelihood of attracting substantial shareholder support.

To date, no company has taken up Atkins’ invitation to seek exclusion of a shareholder proposal on state law grounds under Rule 14a-8(i)(1). As the shareholder proposal landscape continues to evolve, however, some companies may become more willing to explore that avenue during the 2027 proxy season.

Evolution of proponent tactics

Even in the absence of further SEC staff policy changes, shareholder proponents continue to experiment with new ways to pressure companies to advance their objectives. Facing headwinds from the SEC staff’s current no-action policy, declining levels of shareholder support for certain proposal categories and the prospect of a future rescission of Rule 14a-8, proponents have continued to test innovative strategies in 2026, many of which may provide insight into how proponents could seek to maintain influence in a world where Rule 14a-8 plays a diminished role or has been repealed. These strategies include:

- Litigation challenging proposal exclusions.

- Running or threatening Rule 14a-4 “zero slate” campaigns where multiple shareholder proposals are submitted on the proponent’s universal proxy card while sidestepping the parameters of Rule 14a-8 (see, e.g., BJ’s Wholesale Club and Nexstar Media Group in 2026, following a strategy similar to that employed at Warrior Met Coal, as discussed in our 2024 shareholder proposal alert).

- Withhold campaigns targeting directors, threatening to make director elections an alternative forum for E&S and governance activism.

- Public campaigns criticizing companies that exclude proposals or are perceived as insufficiently responsive to shareholder concerns.

- Binding bylaw amendment proposals submitted pursuant to Rule 14a-8 or through independent solicitation efforts.

The 2026 proxy season has been characterized by significant policy changes, strategic experimentation and legal uncertainty, and those dynamics are likely to persist into 2027. The practical effects of SEC skepticism toward shareholder proposals and E&S activism, political and regulatory scrutiny of proxy advisors, and declining support for certain categories of E&S proposals may be offset, at least in part, by evolving proponent strategies and continued uncertainty regarding the future of Rule 14a-8. In this environment, companies should prepare for a range of potential outcomes. Boards and management teams may benefit from ongoing education regarding developments in the shareholder proposal landscape, proactive engagement with shareholders and other key stakeholders, and periodic reassessments of governance and disclosure practices in light of evolving investor expectations and regulatory developments.

[1] Proposal submission and voting figures in this alert accordingly differ from those reported in prior-year alerts.

Related Contacts

This content is provided for general informational purposes only, and your access or use of the content does not create an attorney-client relationship between you or your organization and Cooley LLP, Cooley (UK) LLP, or any other affiliated practice or entity (collectively referred to as "Cooley"). By accessing this content, you agree that the information provided does not constitute legal or other professional advice. This content is not a substitute for obtaining legal advice from a qualified attorney licensed in your jurisdiction, and you should not act or refrain from acting based on this content. This content may be changed without notice. It is not guaranteed to be complete, correct or up to date, and it may not reflect the most current legal developments. Prior results do not guarantee a similar outcome. Do not send any confidential information to Cooley, as we do not have any duty to keep any information you provide to us confidential. When advising companies, our attorney-client relationship is with the company, not with any individual. This content may have been generated with the assistance of artificial intelligence (Al) in accordance with our Al Principles, may be considered Attorney Advertising and is subject to our legal notices.