Comparing the SEC Climate Rules to California, EU and ISSB Disclosure Frameworks

The Securities and Exchange Commission (SEC) adopted its long-awaited climate disclosure rules on March 6, 2024. (For more information, see our recent Cooley client alert, webinar and resource page.) The final rules require US domestic companies and foreign private issuers (FPIs) to disclose qualitative and quantitative climate-related information in their registration statements and periodic reports in general alignment with internationally accepted disclosure frameworks, including the Task Force on Climate-Related Financial Disclosures (TCFD) and the Greenhouse Gas (GHG) Protocol.

Note on ongoing SEC climate rules litigation: On March 15, the US Court of Appeals for the Fifth Circuit granted a motion subjecting the SEC climate rules to an administrative stay pending review of the rules by the court. In addition to litigation in the Fifth Circuit, cases are pending in the Sixth, Eighth and Eleventh Circuits seeking to block the new rules, as well as challenges from environmental groups in the Second and DC Circuits pushing for stronger rules. The Judicial Panel on Multidistrict Litigation will consolidate the challenges before a single court of appeals, which may then dissolve the Fifth Circuit’s order.

While this temporary stay may be of limited long-term effect, companies may need to prepare for compliance with the SEC rules in the shadow of ongoing litigation uncertainty, an expected outcome similar to the conflict minerals rules. The prospect of yearslong litigation likely is most unsettling for companies that do not already publish robust climate disclosures and would not plan to do so in the absence of the SEC rules, though many such companies may not necessarily have extensive disclosure obligations under the SEC’s materiality-focused framework in any case. Litigation uncertainty may be less impactful on compliance planning for companies also subject to California or European Union rules, or that otherwise make extensive voluntary disclosures.

For many companies, however, the SEC climate rules will apply in addition to other mandatory sustainability reporting frameworks already in force or imminently applicable. While the SEC’s climate rules touch on many of the same areas as the three 2023 California climate disclosure laws (Senate Bills 253 and 261 and Assembly Bill 1305) and the EU’s Corporate Sustainability Reporting Directive (CSRD), there are points of significant divergence. The reporting landscape is likely to become increasingly complex, with numerous jurisdictions, including Australia, Hong Kong, Singapore and the United Kingdom, planning to adopt, or having already adopted, legislation to integrate the climate-related disclosure framework developed by the International Sustainability Standard Board (ISSB) – International Financial Reporting Standards (IFRS) S1 and IFRS S2 – into their corporate reporting. As a successor to the TCFD, the ISSB also will be an influential framework for those companies wishing to continue to report sustainability information voluntarily, particularly as institutional investors, such as BlackRock, and other stakeholders integrate these frameworks into their policies and engagement priorities.

In addition, on March 15, 2024, the EU’s Corporate Sustainability Due Diligence Directive (CSDDD) was approved by the Council of the EU. Subject to final approval by the European Parliament, expected in April, the CSDDD will become law and will apply to certain companies as early as 2027. For in-scope US companies, the CSDDD will generate additional climate-related obligations, including a mandatory requirement to adopt and put into effect a climate transition plan that aims to ensure, through best efforts, that their business models and strategies are compatible with the limiting of global warming to 1.5 °C. In addition to potentially impacting SEC climate target and transition plan disclosures, these CSDDD obligations may also impact how companies analyse climate risk and emissions materiality in future SEC disclosure.

Key differences between frameworks

Navigating these regimes can be arduous and companies will need to work to understand the differences to develop an effective cross-regulatory reporting strategy. Later in this alert, we’ve provided a table with a detailed summary of the similarities and differences between these climate reporting frameworks. Key differences include:

GHG emissions

While the SEC has scaled back on requirements for companies to report on their GHG emissions, limiting disclosures to Scopes 1 or 2 where material, the California climate disclosure laws, the CSRD and the ISSB standards all require disclosure of Scope 3 GHG emissions as well as Scopes 1 and 2. While the California climate disclosure laws remain unique in that they require disclosure irrespective of materiality, companies in scope of the CSRD are likely to struggle to avoid disclosing GHG emissions, given the reporting regime’s requirement for double materiality, its broader approach to decision usefulness, and its starting assumption that Scope 3 emissions are an important driver of a company’s transition risk.

Governance, strategy, risk management and targets

Outside of emissions and climate risk, the SEC rules include numerous qualitative and quantitative disclosures related to governance, strategy, risk management, and expenditures that are absent in the California laws and are more akin to those required under the CSRD and ISSB frameworks. While California’s SB 261 also covers material risk disclosure, the SEC rules require additional disclosures of climate-related governance, strategy, transition plans to mitigate or adapt to material climate-related risks, and climate-related financial statement metrics. These SEC qualitative disclosure requirements are consistently linked to material risks and material impacts, such that disclosure on these topics may be broader in certain circumstances under the CSRD and ISSB (or even the California rules with regards to target disclosure under AB 1305, which is not limited to targets expected to have a material impact on reporting companies). This is particularly likely for those in scope of the CSRD, given that certain governance and risk management disclosures are mandatory irrespective of materiality, as well as the CSRD’s broader materiality standard.

Materiality

On paper, materiality standards under the CSRD and SEC and other climate frameworks remain a significant point of divergence. While disclosures under the ISSB, the SEC climate rules and SB 261 are guided by financial or investor materiality (those factors affecting a company’s performance or investor decision-making), the CSRD requires companies to undertake a “double materiality” assessment. This means that companies subject to the CSRD must disclose information on the impacts of their business on the environment and society irrespective of the positive or negative effect of such impacts on companies’ financials. It remains to be seen, however, whether in practice double materiality will significantly impact disclosures, as stakeholder impacts, such as significant environmental or negative community externalities, can often result in financial risks. Unlike the SEC rule, the CSRD also requires companies to disclose how their quantitative and qualitative materiality thresholds have been set and applied. Once a topic, such as climate, is determined to be material, disclosure of particular information under such a topic is defined by decision usefulness, which includes usefulness to users such as civil society, non-governmental organizations, governments, analysts and academics, representing a much broader standard than SEC materiality. Disclosures under California’s SB 253 and AB 1305, by contrast, are mandatory irrespective of materiality, though SB 253 reporting is expected to be clarified by future implementing regulations by the California Air Resources Board.

Looking beyond climate and the company

Beyond materiality, the EU’s CSRD is an outlier both in terms of the number of sustainability topics covered beyond climate, and its broad value chain reporting mandates, as companies must report not only on their own activities but also on the sustainability-related impacts, risks, and opportunities in their upstream and downstream value chains. While only those disclosure requirements for EU entities and their groups have been published to date, the sustainability topics covered include water and marine resources, biodiversity, workers in the value chain, and the circular economy. (For more information, refer to our August 2023 client alert.)

Practical implications for SEC-registered companies

As a result of the above-discussed differences, multiframework reporting will present important practical implications for SEC-registered companies, including:

Emissions reporting will be unavoidable for many companies

Scope 3 reporting will be required for companies subject to SB 253 and, in practice, is likely unavoidable under the CSRD, despite such disclosures being abandoned in the final SEC rule, and under SB 253, Scopes 1 and 2 reporting also will not be subject to materiality tests. As a result, the changes to the SEC emissions reporting requirements may be much less consequential, even if companies may still avoid the added burden of including such disclosures in SEC filings. In addition, even when emissions reporting is not subject to materiality tests, emissions reporting under the GHG Protocol, particularly Scope 3, is shaped by judgments as to the materiality of emission types.

Companies may adopt more rigor in California, CSRD or voluntary reporting

Given overlap with SEC regulations, companies may approach California, EU, ISSB or other voluntary climate reporting with greater disclosure controls, including legal and internal audit oversight. In addition to potentially influencing SEC reporting decisions, public disclosures in other reports on a topic covered by SEC rules may increase a company’s exposure to SEC enforcement or inquiries, liability under the US federal securities laws, and general investor scrutiny.

Disclosures in California, CSRD or ISSB reports may impact SEC disclosure strategies

Companies that otherwise may have attempted to treat their emissions or climate targets as nonmaterial may be less likely to do so if already required to disclose such matters under other regulations, though many companies may be reluctant to take on the added liability and other risks of disclosure in SEC filings. CSRD disclosures also may impact how companies approach materiality for SEC purposes. Although climate reporting under the CSRD is subject to a materiality test, the CSRD requires certain detailed climate-related disclosures irrespective of materiality. It is mandatory to disclose a company’s processes, including its use of scenario analysis, to identify and assess climate-related impacts, risks, and opportunities.

In addition, under the CSRD if a company determines that it will not report on climate, it must nevertheless publish a detailed justification as to why the climate-related information is not material enough, from both a financial and impact perspective, to require reporting, including a forward-looking analysis of the conditions that could lead the undertaking to conclude that climate change is material in the future. The combination of the CSRD’s mandatory climate disclosures and its double materiality standard is expected to result in widespread decisions to fully report on climate, including emissions. The extensive disclosures required under the CSRD, including on the materiality analysis, may make it more difficult for companies to justify determinations that climate risks or emissions are nonmaterial, or to avoid SEC comments.

SEC implications may drive voluntary reporting strategies

Companies that wish to minimize the inclusion of climate-related disclosures in SEC filings may now have an incentive to minimize voluntary actions that could attract SEC or investor scrutiny of materiality determinations, such as voluntary climate-related disclosures in voluntary sustainability reports under the ISSB or other frameworks, or the publicizing of climate-related targets and goals. It is yet to be seen, however, whether rating agencies, institutional investors, corporate customers or other stakeholders, who often drive voluntary reporting strategies, will drop requirements for companies to provide disclosures under voluntary sustainability standards, such as Carbon Disclosure Project (CDP).

SEC implications may influence CSRD reporting strategies

Most US businesses that are in scope of the CSRD will be filing reports first at their EU subsidiary level in 2026 and later at the level of the ultimate US parent company in 2029. Many such companies are nevertheless considering early consolidated reporting at the ultimate parent-level for practical reasons. The appeal of early parent-level reporting may be impacted by the publication of the SEC rules, to avoid publishing materiality, risk, emissions, or other parent-level disclosures that may influence SEC reporting or attract SEC scrutiny. Nonetheless, there will not always be significant differences parent and subsidiary-level climate reporting under the CSRD, particularly with respect to Scope 3 emissions, so companies will need to make circumstances-specific judgements.

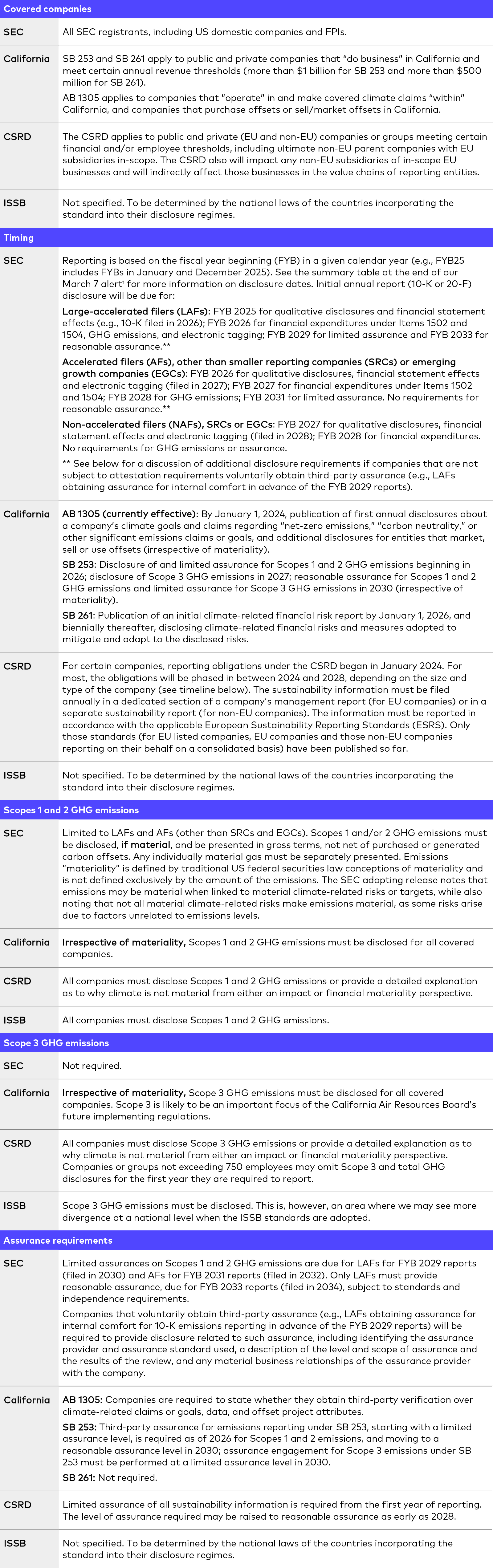

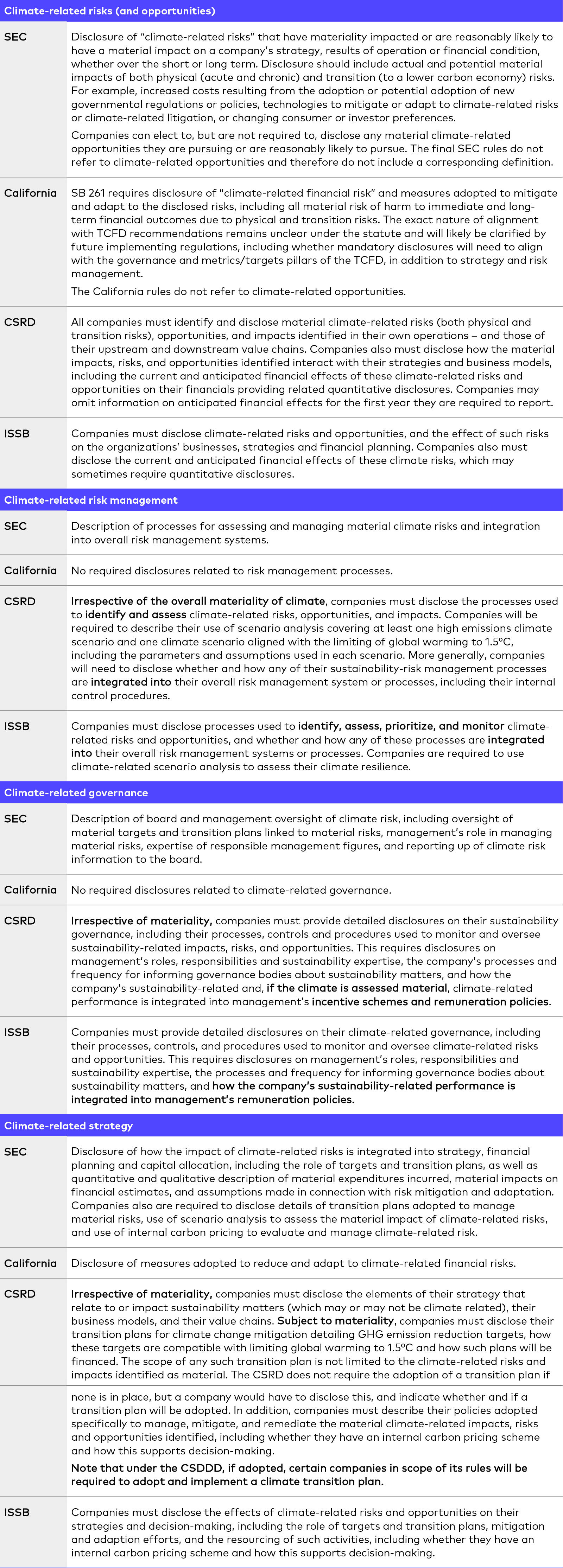

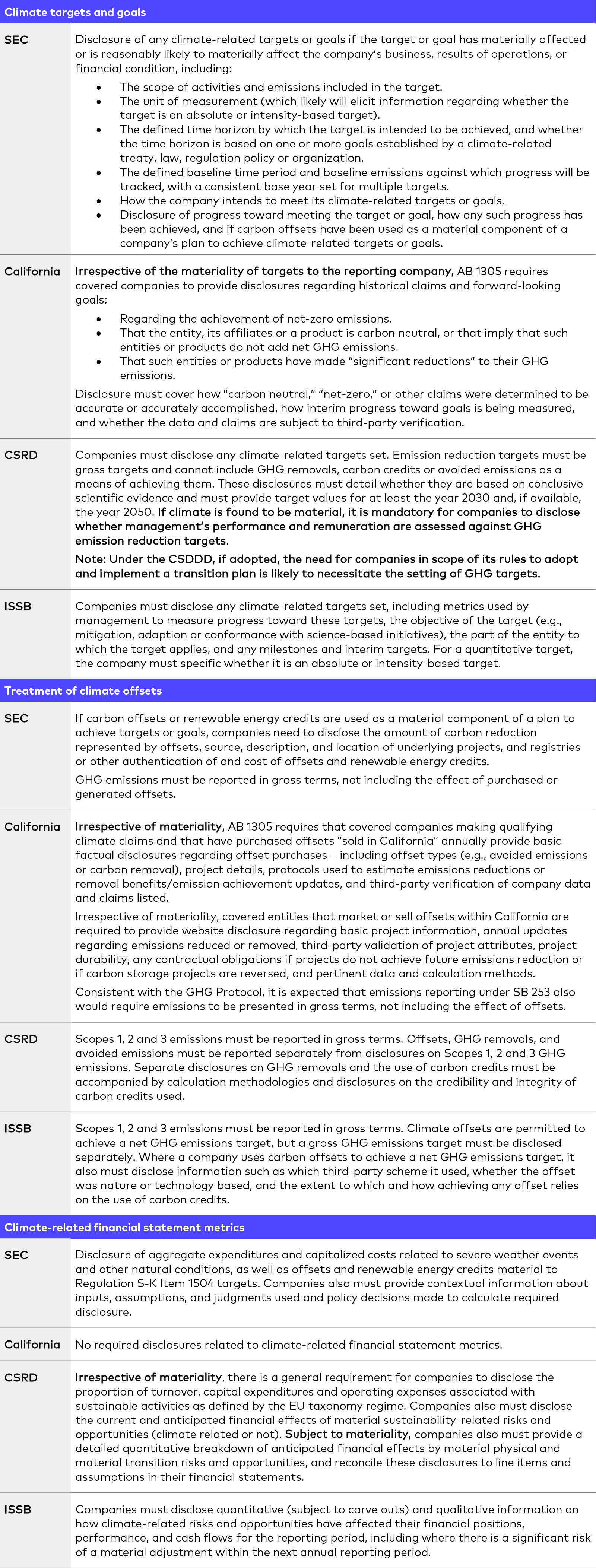

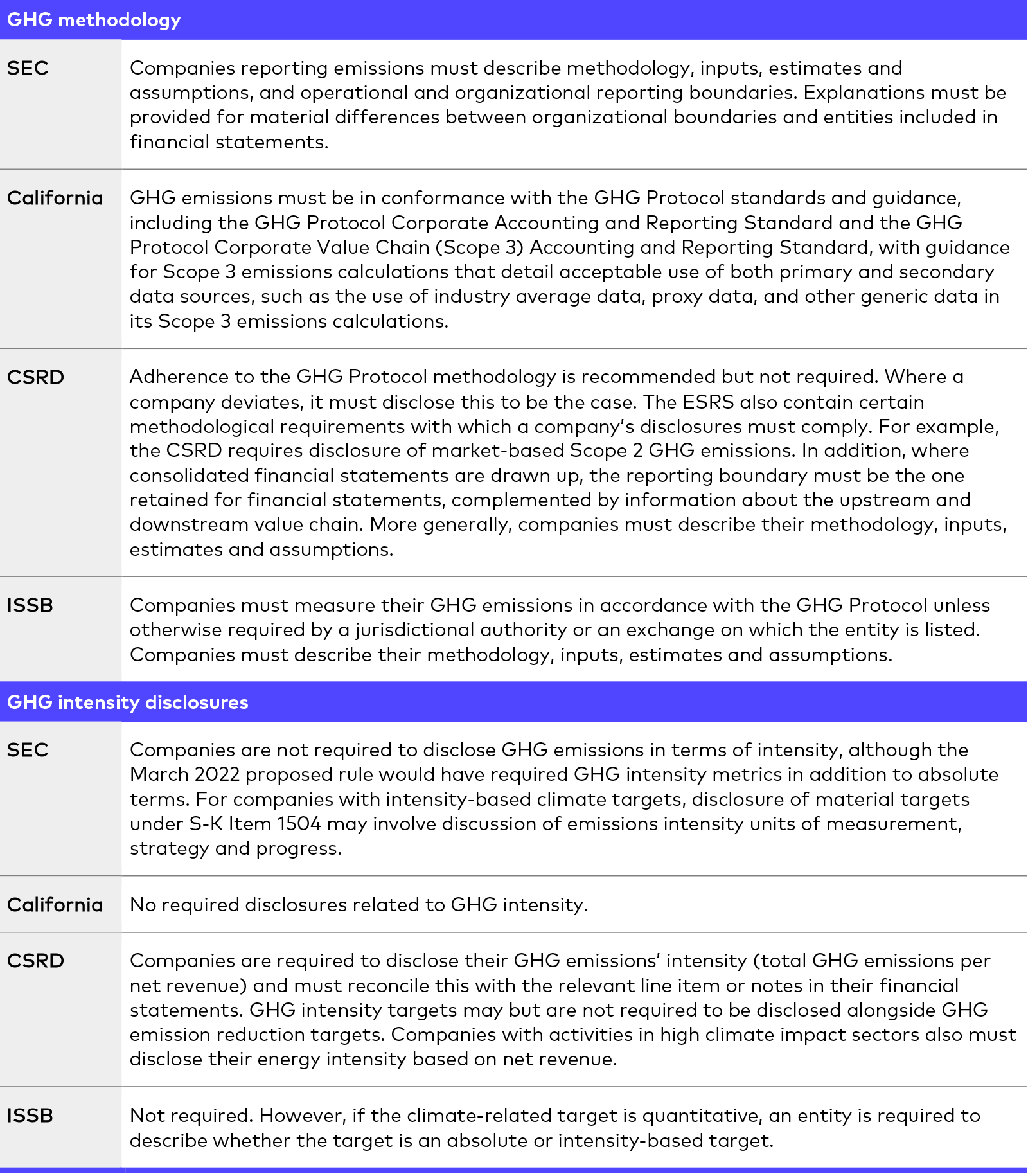

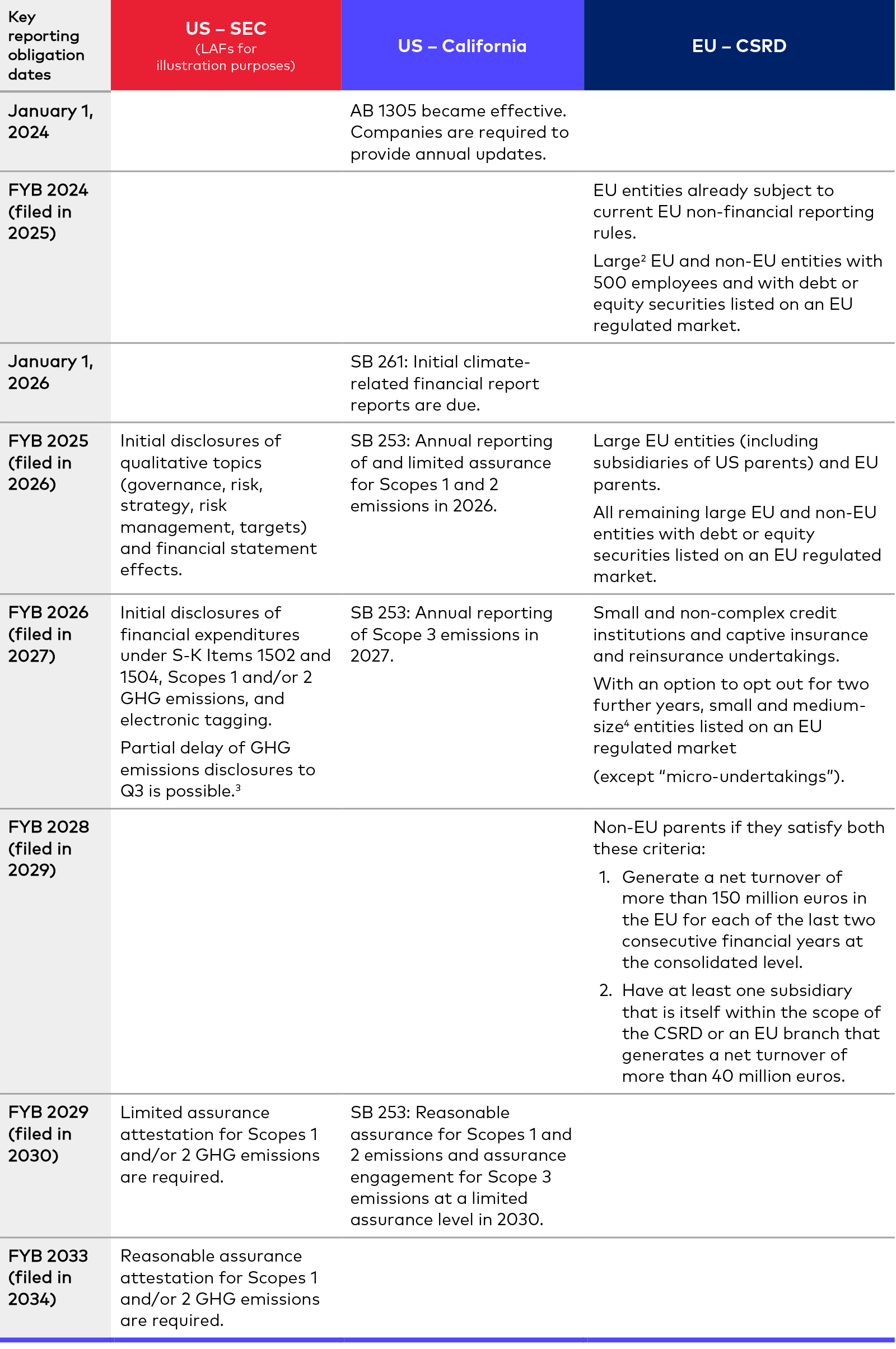

Disclosure framework comparison

Below is a high-level comparison of the SEC climate rules, the three California climate disclosure laws, the CSRD* and ISSB.

* The commentary on the CSRD is limited to the ESRS published to date, which apply predominantly to EU companies, their groups and those with securities admitted to trading on EU regulated markets. Further sector-specific standards that also will apply are expected. The reporting standards for ultimate non-EU parents required to report under the CSRD have not yet been published, but they are not expected to be as detailed as those described in this alert and are likely to be focused on sustainability impacts, rather than sustainability-related financial risks and opportunities. For more information, see Cooley’s FAQ on the CSRD.

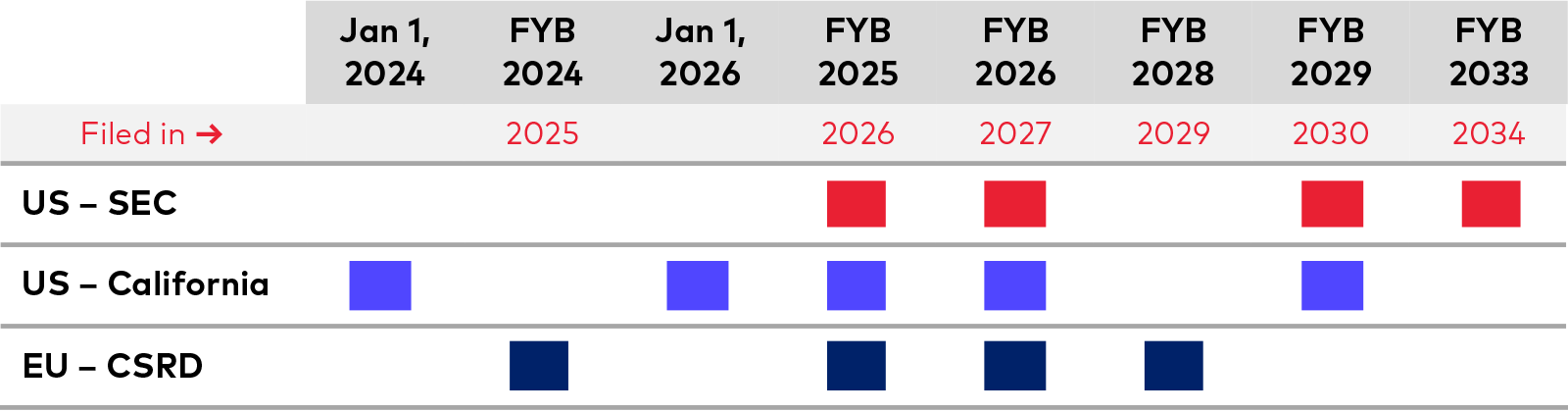

Which entities need to comply and from when?

Notes

The tables estimate filing dates based on FYB January 1 and present compliance dates for SEC LAFs, as these are the filers most likely to be subject to the CSRD, SB 253 and SB 261.

- See the summary table at the end of our March 7 alert for more information on disclosure dates.

- Entities that on an individual or, if a group, consolidated basis satisfy at least two of the following: (1) balance sheet total of more than 25 million euros; (2) net turnover of more than 50 million euros; (3) an average of more than 250 employees during the financial year.

- Entities that are not large and on an individual or, if a group, consolidated basis satisfy at least two of the following: (1) balance sheet total of more than 450,000 euros; (2) net turnover of more than 900,000 euros; (3) an average of more than 10 employees during the financial year.

- To allow for additional time to prepare emissions data, disclosure of GHG emissions data may be incorporated into a company’s second quarter 10-Q or filed in a 10-K/A by the filing deadline for the second quarter 10-Q. For FPIs, GHG emissions data is due in a 20-F/A no later than 225 days after the fiscal year-end. In each case, to take advantage of this delay, the issuer must include a statement in its annual report on Form 10-K or 20-F, as applicable, to indicate its express intention to later amend its filing to make these GHG emissions disclosures.

Related Contacts

This content is provided for general informational purposes only, and your access or use of the content does not create an attorney-client relationship between you or your organization and Cooley LLP, Cooley (UK) LLP, or any other affiliated practice or entity (collectively referred to as "Cooley"). By accessing this content, you agree that the information provided does not constitute legal or other professional advice. This content is not a substitute for obtaining legal advice from a qualified attorney licensed in your jurisdiction, and you should not act or refrain from acting based on this content. This content may be changed without notice. It is not guaranteed to be complete, correct or up to date, and it may not reflect the most current legal developments. Prior results do not guarantee a similar outcome. Do not send any confidential information to Cooley, as we do not have any duty to keep any information you provide to us confidential. When advising companies, our attorney-client relationship is with the company, not with any individual. This content may have been generated with the assistance of artificial intelligence (Al) in accordance with our Al Principles, may be considered Attorney Advertising and is subject to our legal notices.