SEC Adopts Climate Reporting Requirements

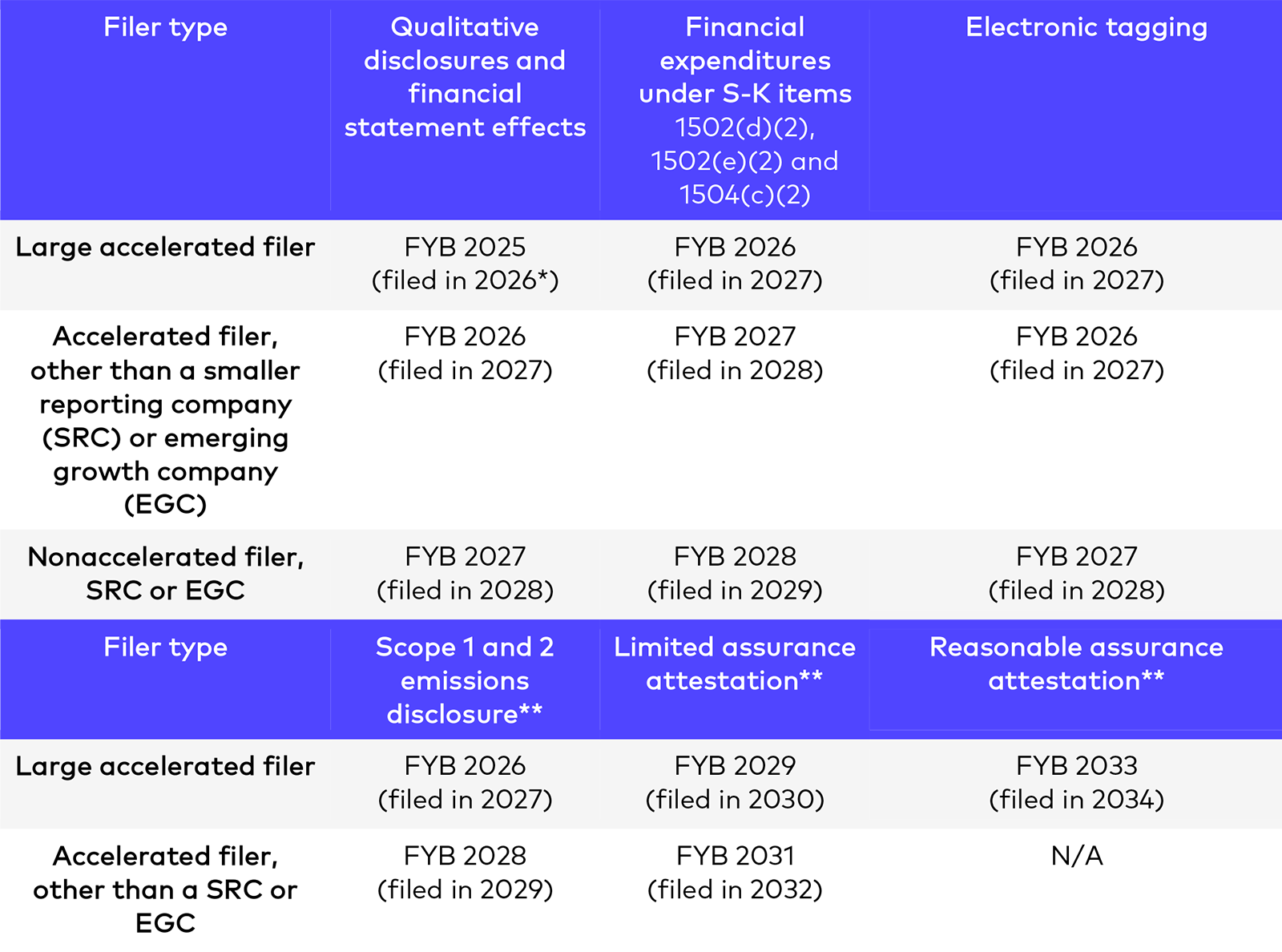

On March 6, 2024, the Securities and Exchange Commission (SEC) voted at an open meeting to adopt final rules to mandate climate-related disclosure by public companies. The long-awaited rules will require qualitative disclosure on climate risk, risk management, governance and targets, as well as quantitative emissions and expenditure reporting requirements under certain circumstances. Initial disclosures under the final rules for large accelerated filers will be due in 2026, with emissions and financial expenditures disclosures due in 2027. Please see the summary table at the end of this alert for more information on disclosure dates, including for other filers.

This initial publication will be followed by subsequent articles exploring the final climate rules in more detail, including their relationship to the California and European Union (EU) rules. Cooley also hosted a webinar on March 12 to discuss the final rules, as well as key questions and next steps for issuers, which you can view on demand. For more resources related to the climate rules, please visit our ESG Resources page.

While the adopted qualitative disclosure requirements are broadly consistent with the proposed requirements, the final rules introduce numerous significant changes with respect to emissions reporting and attestations that are intended to reduce reporting burdens on many companies and provide increased breathing room for disclosure preparation. SEC Chair Gary Gensler, in his prepared remarks, noted several times that the adopted rules are “grounded in materiality,” and almost all the new disclosure requirements will be subject to a materiality determination, in line with other parts of Regulation S-K. Of particular note, the final rules limit Scope 1 and 2 greenhouse gas (GHG) emissions reporting to material emissions and generally link climate expenditure, strategy, transition plans and targets disclosures to material risks and impacts. Additionally, the final rules do not include Scope 3 emissions reporting requirements and allow for significant phase-in periods for attestations of Scope 1 and 2 GHG emissions. The final rules also pare back the financial statement disclosure from the proposed rule by removing the requirement to disclose the impact of climate-related events on each line item of a company’s financial statements.

The SEC published its initial climate rule proposal on March 21, 2022, which went on to generate more than 24,000 comments from the public, in addition to extensive congressional, media and industry coverage. Adoption of the final rules was delayed several times, during which period other climate-related disclosure rules were published in the US and other jurisdictions. These include three climate reporting laws in California (SB 253, SB 261 and AB 1305) and the Corporate Sustainability Reporting Directive (CSRD) framework in the EU. Although the SEC’s modified emissions reporting requirements will likely be met with some relief for many issuers, as well as nonpublic companies in issuers’ value chains, the impact of these changes will be significantly blunted due to the broad Scope 1, 2 and 3 emissions reporting requirements under the California and EU rules, which are expected to apply to thousands of US companies.

Disclosure will be required for both domestic and foreign private issuers in annual reports on Forms 10-K and 20-F, as applicable, as well as in registration statements under the Securities Act. The climate rules will apply similarly to foreign private issuers, except that an issuer that files consolidated financial statements under International Financial Reporting Standards (IFRS) as issued by the International Accounting Standards Board (IASB) would apply IFRS as the basis for calculating and disclosing the financial statement metrics rather than US generally accepted accounting principles (GAAP). Foreign private issuers that qualify to use the Multijurisdictional Disclosure System (MJDS) and file annual reports on Form 40-F are exempt from the final climate-related disclosure rules.

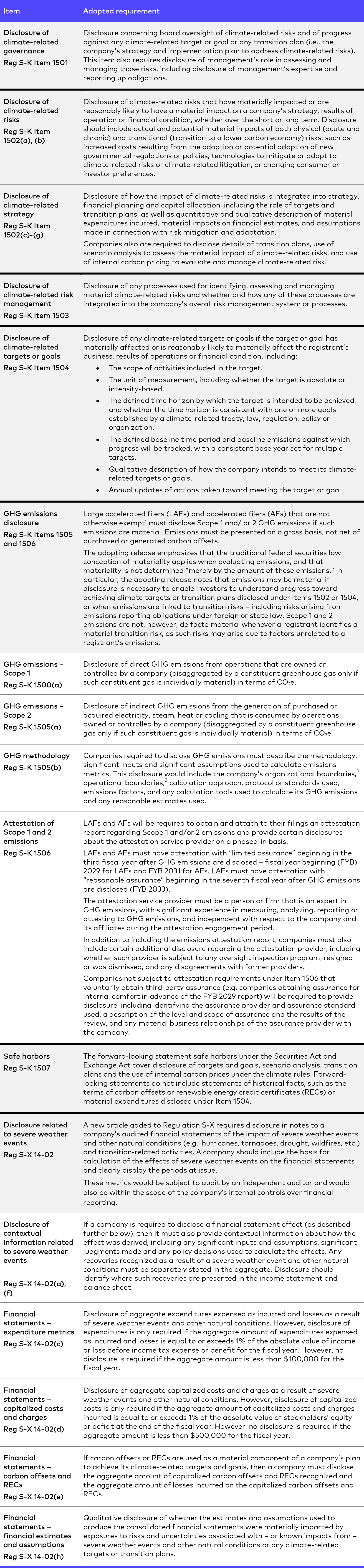

The table below provides a high-level summary of the emissions and qualitative disclosure requirements under the new Regulation S-K Item 1500, as well as the financial statement disclosure requirements under the new Regulation S-X Article 14.

Disclosure compliance dates

Reporting requirements under the climate rules are based on fiscal years beginning in a given calendar year – or “FYBs.” For example, FYB 2025 would include fiscal years beginning on January 1 through December 31, 2025.

* All filing dates assume December 31 fiscal year-ends.

** To allow for additional time to prepare emissions data, disclosure of GHG emissions data may be forward incorporated into a company’s second quarter 10-Q or filed in a 10-K/A by the filing deadline for the second quarter 10-Q. For foreign private issuers, GHG emissions data is due in a 20-F/A no later than 225 days after the fiscal year-end. In each case, to take advantage of this delay, the issuer must include a statement in its annual report on Form 10-K or 20-F, as applicable, to indicate its express intention to later amend its filing to make these GHG emissions disclosures.

The new rules will become effective 60 days after publication in the Federal Register. Companies will be required to comply with the new rules based on filer status. For detailed information regarding filer status determination, refer to Cooley’s Guide to Determining Securities Exchange Act Filer and Smaller Reporting Company Status.

Notes

- AFs that are smaller reporting companies or emerging growth companies are not required to provide GHG emissions disclosure.

- “Organizational boundaries” refer to the company’s determination of the boundaries that define the operations that it owns or controls for purposes of calculating GHG emissions. If such boundaries materially differ from the scope of entities and operations included in a company’s consolidated financial statements, the rules will require a brief explanation of this difference.

- “Operational boundaries” refer to the boundaries that determine the direct and indirect emissions associated with the business operations owned or controlled by a registrant.

Related Contacts

This content is provided for general informational purposes only, and your access or use of the content does not create an attorney-client relationship between you or your organization and Cooley LLP, Cooley (UK) LLP, or any other affiliated practice or entity (collectively referred to as "Cooley"). By accessing this content, you agree that the information provided does not constitute legal or other professional advice. This content is not a substitute for obtaining legal advice from a qualified attorney licensed in your jurisdiction, and you should not act or refrain from acting based on this content. This content may be changed without notice. It is not guaranteed to be complete, correct or up to date, and it may not reflect the most current legal developments. Prior results do not guarantee a similar outcome. Do not send any confidential information to Cooley, as we do not have any duty to keep any information you provide to us confidential. When advising companies, our attorney-client relationship is with the company, not with any individual. This content may have been generated with the assistance of artificial intelligence (Al) in accordance with our Al Principles, may be considered Attorney Advertising and is subject to our legal notices.