EU Changes CSRD Thresholds to Reduce Sustainability Reporting Burden

Check whether this impacts your business

In January 2023, the European Union adopted the Corporate Sustainability Reporting Directive (CSRD), which requires EU and non-EU companies meeting certain thresholds to file annual sustainability reports alongside their financial statements. On 17 October 2023, the European Commission adopted an amendment to the thresholds in the Accounting Directive, impacting which entities will need to file CSRD-compliant reports.

What are the adjusted thresholds?

A company’s reporting obligations under the CSRD are determined by the size of the company or group. Most large EU companies and groups will need to comply for financial years beginning on or after 1 January 2025, and certain small and medium-sized enterprises (SMEs) will need to comply for financial years beginning on or after 1 January 2026.

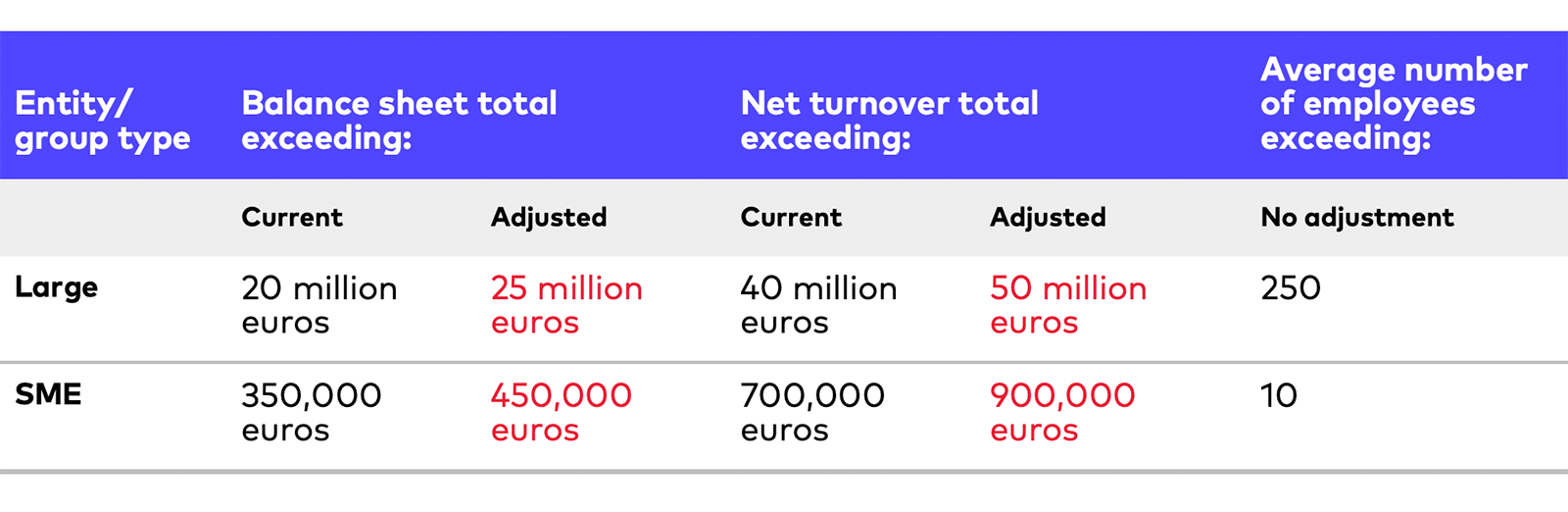

A comparison of the current and new thresholds is set out in the table below

Threshold test for non-EU parent companies

The threshold for non-EU parent companies to prepare a group report under the CSRD from financial year beginning on or after 1 January 2028 has not been adjusted. The CSRD remains applicable to any non-EU company which satisfies both of the following criteria:

- Generates a net turnover of more than 150 million euros in the EU for each of the last two consecutive financial years at the consolidated level (or, if not applicable, at the individual level).

AND

- Has at least one EU subsidiary in scope of the CSRD, or has at least one branch which generated a net turnover of more than 40 million euros in the preceding financial year.

When will these adjusted thresholds apply?

Member states are required to apply these new thresholds for financial years beginning on or after 1 January 2024. Member states may, however, allow entities to apply these adjusted thresholds for financial years starting on or after 1 January 2023. This will be determined at the individual member state level.

Why have the thresholds been changed?

The stated reason for raising the thresholds is to accommodate for inflation over the past 10 years and reduce the reporting burden for smaller companies.

Next steps

The amendments adopted by the European Commission are now subject to a scrutiny period (usually two months, although this can be extended) during which the European Parliament or European Council might veto the changes. If the changes are not vetoed, the amendments will be formally published in the Official Journal of the European Union and will enter into force three days after.

Are there any other changes on the horizon?

No changes to the first set of European Sustainability Reporting Standards (ESRS): The ESRS which will start to apply to certain large EU companies reporting on FY 2024 also are nearing the end of their cooling off period. Adopted in July 2023, the ESRS are subject to a two-month scrutiny period in the European Parliament and European Council before they formally enter into force at the end of this year. A motion tabled last week to reject the ESRS and requesting a less onerous set of reporting standards was itself rejected on 18 October 2023.

Delays to drafts of the sector-specific and non-EU-specific ESRS: The European Commission’s 2024 Commission Work Programme indicates that it plans to postpone the adoption of sector-specific ESRS and the ESRS to be used by non-EU companies in scope of the CSRD. Adoption of these standards was initially scheduled for June 2024. The proposed two-year delay is not, however, currently expected to impact the reporting deadlines for either EU or non-EU companies in scope of the CSRD.

For further details on the CSRD, see Cooley’s related August 2023 client alert.

If you have any questions or would like support adjusting to this new reporting regime, please contact a member of Cooley’s international ESG & sustainability advisory team.

Related Contacts

This content is provided for general informational purposes only, and your access or use of the content does not create an attorney-client relationship between you or your organization and Cooley LLP, Cooley (UK) LLP, or any other affiliated practice or entity (collectively referred to as "Cooley"). By accessing this content, you agree that the information provided does not constitute legal or other professional advice. This content is not a substitute for obtaining legal advice from a qualified attorney licensed in your jurisdiction, and you should not act or refrain from acting based on this content. This content may be changed without notice. It is not guaranteed to be complete, correct or up to date, and it may not reflect the most current legal developments. Prior results do not guarantee a similar outcome. Do not send any confidential information to Cooley, as we do not have any duty to keep any information you provide to us confidential. When advising companies, our attorney-client relationship is with the company, not with any individual. This content may have been generated with the assistance of artificial intelligence (Al) in accordance with our Al Principles, may be considered Attorney Advertising and is subject to our legal notices.